Aimia (TSX: AIM): Ready for Takeoff

The beginning of a permanent compounding machine.

Not investment advice: First, read my full disclaimer here.

*Numbers in CAD unless otherwise noted.

Rhys Summerton is not a name many have heard of. He’s a South African who founded and operated Milkwood Capital (UK based) over the past decade (previously MD at Citi EM research). This has led him to take several activist stakes that have resulted in strong shareholder outcomes.

His playbook is pretty simple: identify good businesses in a fragmented market that are beat up for one reason or another, strip out all the excess costs / bloat, buy back shares on the cheap and compound through inexpensive, small acquisitions / add ons. Rinse and repeat. Mostly I’ve invested alongside him in several South African investments (more on this, shortly).

However, this walk through is about a C$250M market cap company that trades on the TSX, Aimia. Serving as the Executive Chairman, he’s using this as a permanent capital vehicle. If you’re new to the name and like to be patient with your capital, I think you’ll find the set-up interesting.

Furthermore, in their recent AGM, Aimia gave five company examples that are in their acquisition pipeline. Doing some scuttlebutt, I think I’ve been able to identify a few of these (I’m invested in two of them).

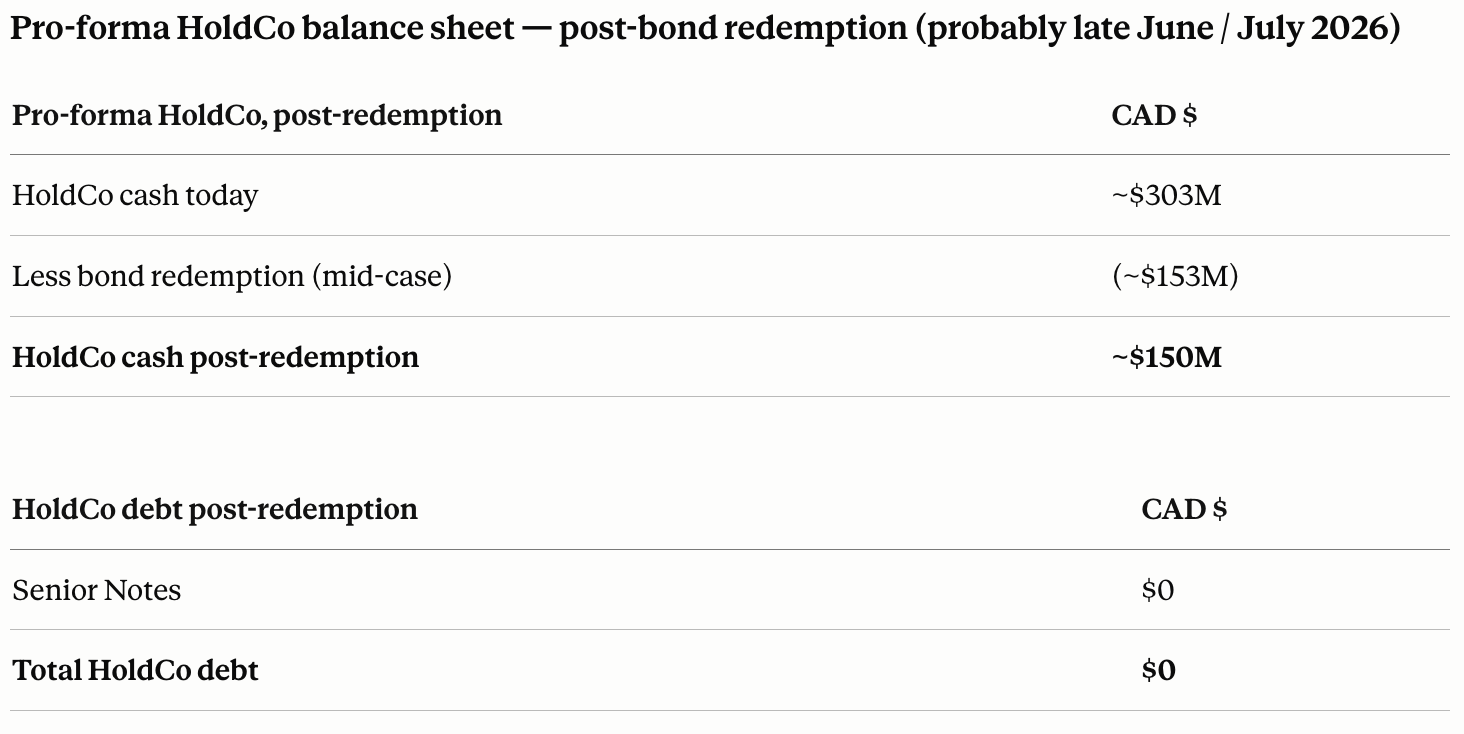

Aimia was originally Air Canada’s loyalty-program holding company. It trades at roughly 80 cents on the dollar to book value while sitting on CAD $1+ billion in tax losses it carries off balance sheet. Recently closing a transaction on May 29th, Rhys is sitting on ~CAD $150 million of cash to enable the start of his acquisition playbook. Many of these targets are serial acquirer platforms that have a long tail of acquisition potential as they mop up fragmented markets - this should result in a clear path to growth for years to come. Meanwhile, the cash they throw off will be protected because of the massive tax losses they have at their disposal.

Buy an attractive platform → Generate cash → Reduce share count → Buy small, inexpensive add-ons

A Brief History:

Aimia began life as Aeroplan, Air Canada’s frequent-flyer program. It was spun out and listed in 2005 as the Aeroplan Income Fund, became Groupe Aeroplan, and rebranded to Aimia in 2011. For most of the next decade it was a loyalty-and-analytics business.

The defining event came in 2019, when Aimia sold the Aeroplan loyalty business back to Air Canada. The headline cash consideration was approximately CAD $450 million, with total transaction value reported closer to CAD $516 million. That sale turned Aimia into a cash-rich shell with no core operating business, resulting in a pivot to become an investment holding company.

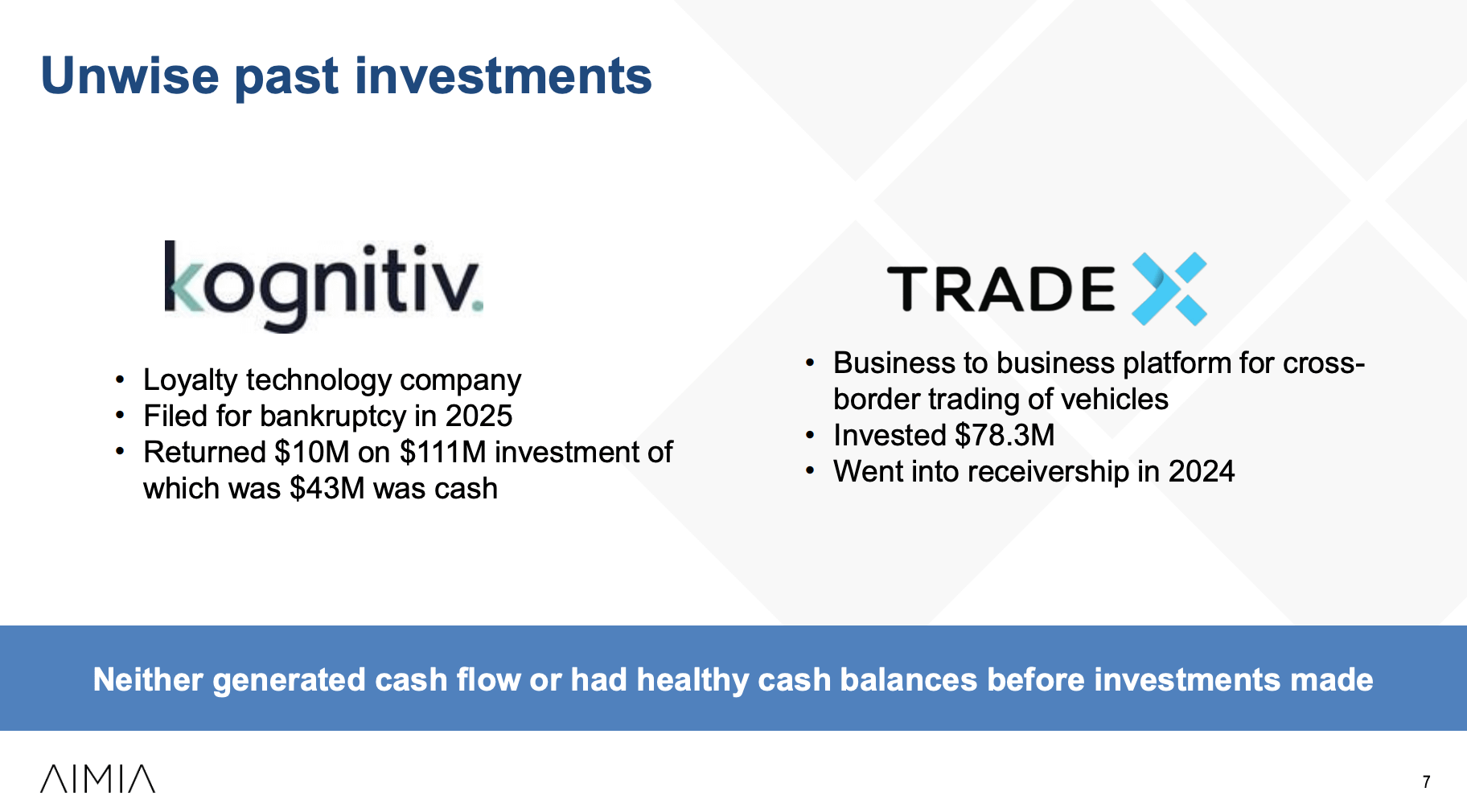

The reinvention did not go smoothly. Under the leadership of brothers Phil and Chris Mittleman, Aimia made a series of investments. A specialty chemicals business (Bozzetto), a synthetic-rope manufacturer (Cortland), stakes in Clear Media, Kognitiv, TRADE X and others. I found this to be a lol slide from the AGM:

That discount attracted an activist. Mithaq Capital, a Saudi based family office (one of the richest non-royal families), accumulated a large stake and, at the April 2023 annual meeting, ran a “vote no” campaign that toppled the chair with no director clearing support needed to retain a seat. Mithaq followed with a hostile all-cash bid at CAD $3.66 per share in October 2023. Aimia’s board resisted, including initiating a defensive private placement that drew a challenge before the Ontario Capital Markets Tribunal. After more than a year of litigation and acrimony, the two sides settled in late 2024: Mithaq took board representation, the lawsuits ended, and the company’s direction shifted decisively toward disciplined, value-oriented capital allocation.

The Aimia that emerges is a holding company with a cleaned-up board, a large and capable controlling shareholder, a portfolio being actively rationalized, and an enormous pool of tax assets accumulated through years of losses and write-downs.

Rhys Summerton:

Aimia’s most important asset does not appear on its balance sheet. It is the person now running it.

Rhys Summerton spent the start of his career at Citigroup, where he was a Managing Director and ultimately Global Head of Emerging Market Equity Research. In 2013 he left to found the Milkwood Fund (the vehicle of Milkwood Capital) a UK-based, globally mandated, highly concentrated value fund that is not shy about activism in smaller companies. Here is a good article about Rhys and Milkwood.

An example of Rhys’s work is embodied by Argent Industrial (JSE: ART), a company I own. Milkwood’s engagement with management is credited with helping spark one of the most impressive value-creation stories in South African small-caps. Argent transformed itself from a low-return domestic steel trader into a globally diversified, cash-generative, debt-free industrial group, retired roughly 43% of its share count, and compounded earnings per share at around 30% a year. Summerton helped drive the capital allocation while the CEO (Treve Hendry) ran point on operations.

Summerton joined Aimia’s board on January 28, 2025, and was subsequently appointed Executive Chairman. Per the 2026 AGM materials, insiders and the board control roughly 42.6% of the shares (~12% for Milkwood and ~30% for Mithaq). You are betting alongside a concentrated value investor with a great track record, a board that owns nearly half the company, and a controlling shareholder in Mithaq. This alignment is what I look for.

The Balance Sheet: NAV, the Bozzetto Sale, and the discount

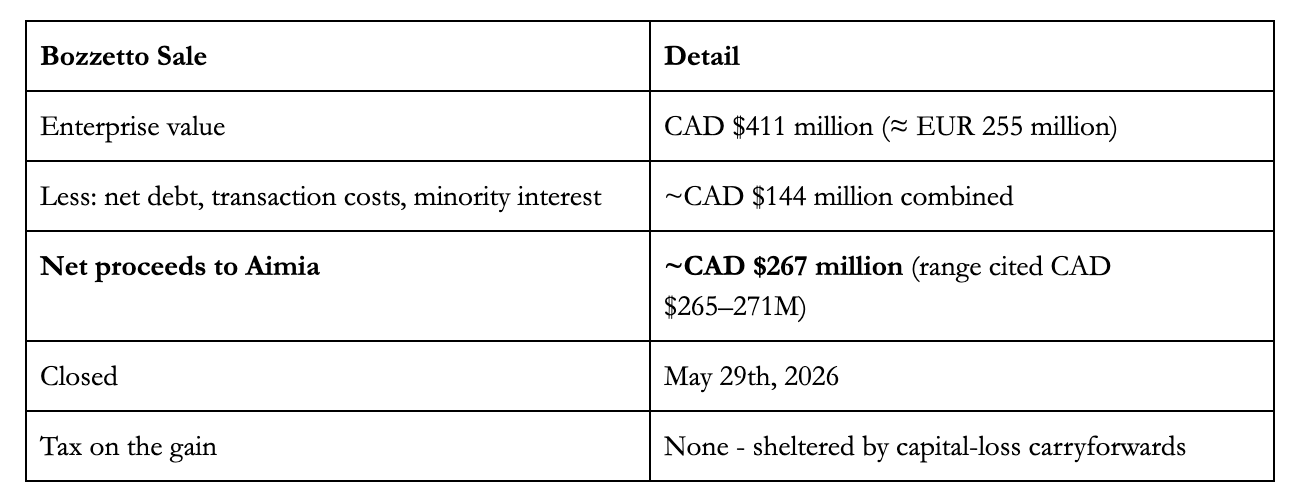

On February 9, 2026, Aimia announced the sale of Giovanni Bozzetto S.p.A., the Italian specialty chemicals business in which it held a 94% interest. The terms:

Post transaction, I think the balance sheet will end up looking like this:

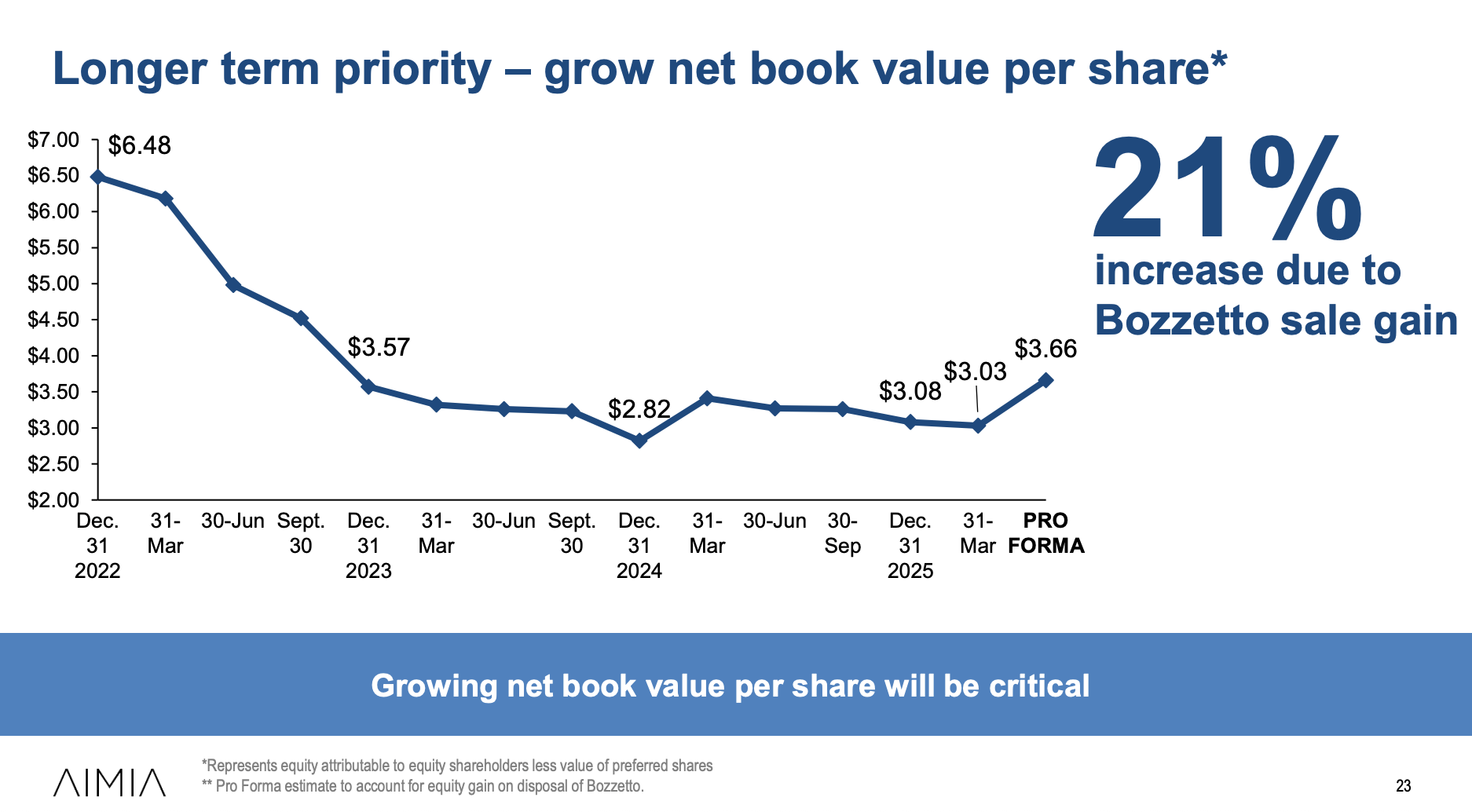

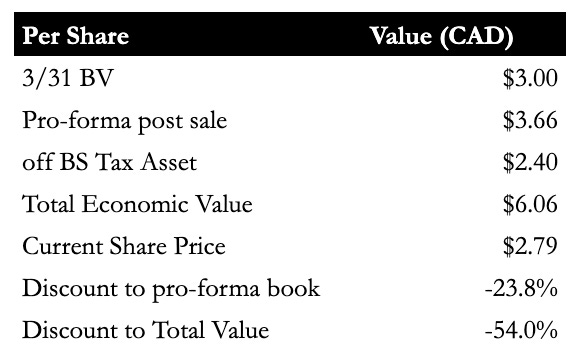

Now the valuation. Aimia’s 2026 AGM presentation reports net book value per common share of CAD $3.66.

Aimia (TSX: AIM) Share price: CAD $2.79 x 89.4M shares = $250M

Pro-forma Net book value / share (Mar 31, 2026): CAD $3.66 (ironically, this is what Mithaq tried to buy them for back in 2023)

Discount to pro-forma book: ~23%

A discount is not unusual for a holding company. Considering the capital allocator at the helm and off balance sheet tax losses, I think the gap is excessive.

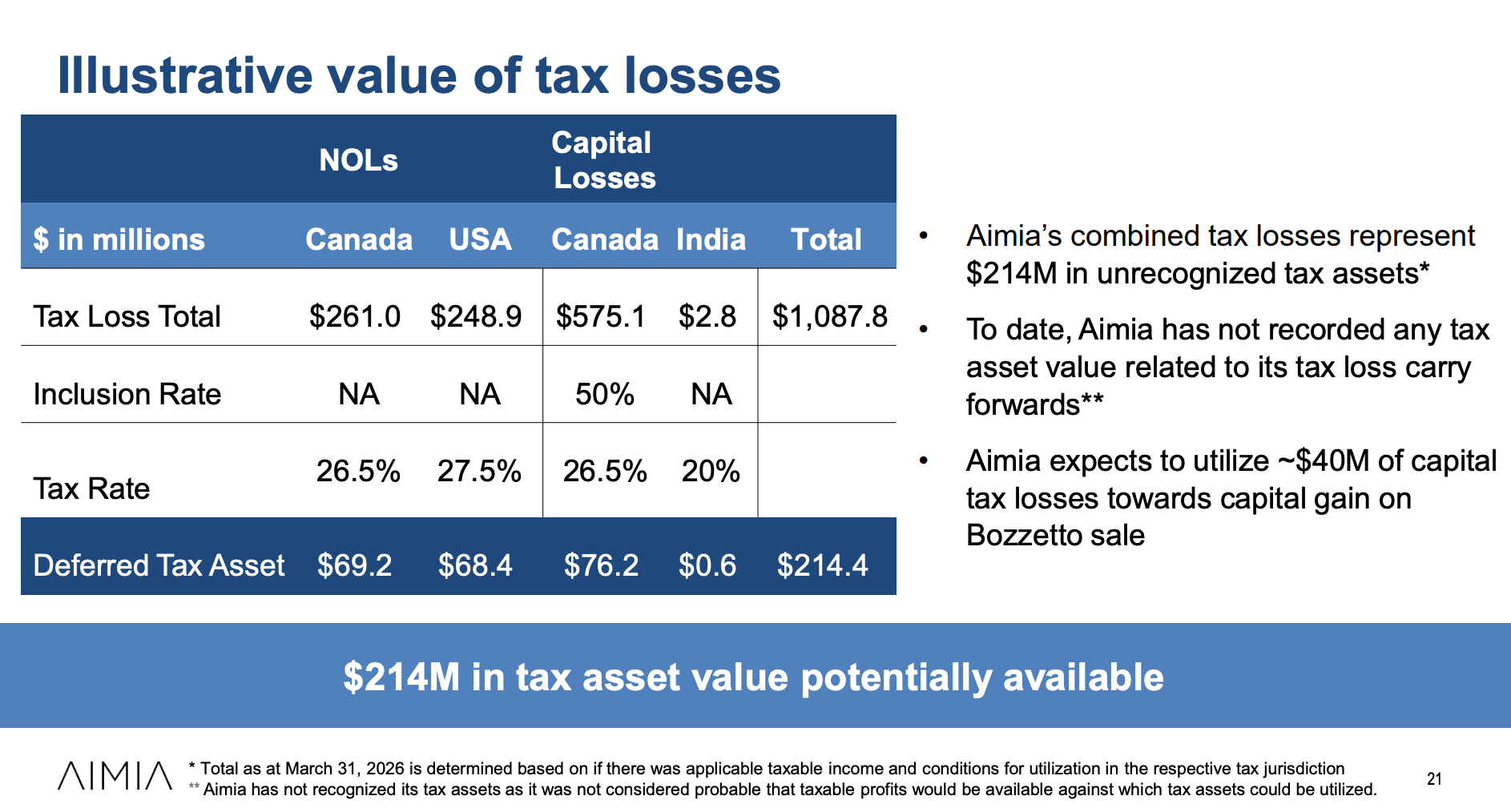

The CAD $1.09 Billion Asset That Isn’t on the Balance Sheet

This is the most under-appreciated element of the Aimia story.

As at March 31, 2026, Aimia carried CAD $1,087.8 million of tax-loss carryforwards:

Aimia has recognized none of this on its balance sheet. Under IFRS, a company may only book a deferred tax asset for losses when it is “probable” that future taxable profit will exist to absorb them. This is the same situation for my last write-up (that also trades sub 2x EV/EBITDA). Aimia’s auditors have not been willing to call that probable, so the entire CAD $1.09 billion sits off balance sheet.

The company’s own AGM materials put an illustrative value of roughly CAD $214.4 million on these unrecognized losses - composed of Canadian and US operating-loss benefits and Canadian and Indian capital-loss benefits. On ~89.4 million shares, CAD $214 million is about CAD $2.40 per share of value that does not appear in the CAD $3.66 book value.

The distinction between “on” and “off” balance sheet is the whole game here:

On balance sheet: none. The CAD $3.66 book value you are buying at a discount excludes the tax assets entirely.

Off balance sheet: the full CAD $1.09 billion. As Aimia acquires profitable operating companies and as it realizes capital gains, those losses convert into cash-tax savings. The Bozzetto sale is an example where Aimia expects to apply roughly CAD $40 million of capital losses against the Bozzetto gain and pay no tax on the disposal.

Cortland - The Remaining Operating Business (and potential write-down)

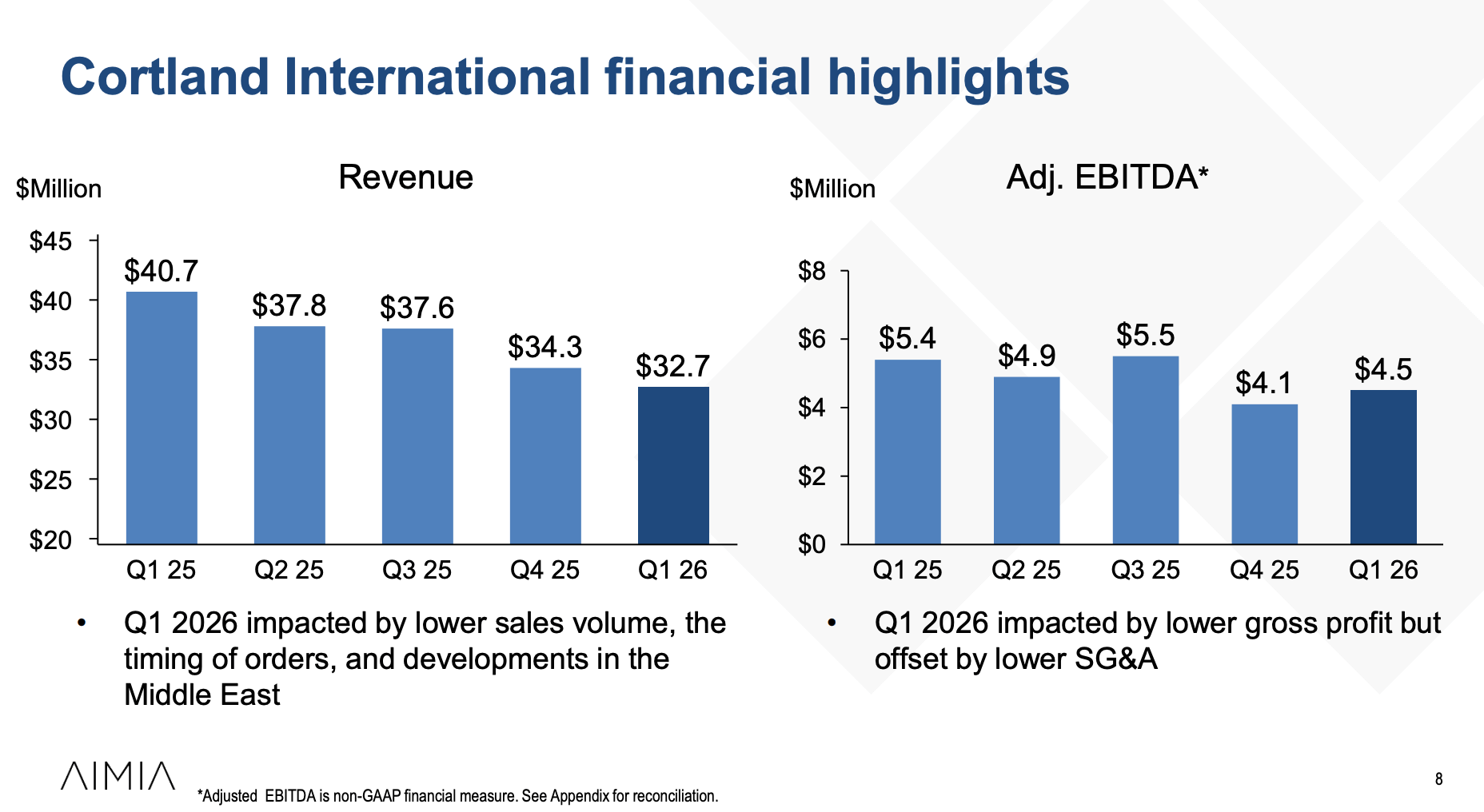

Cortland International is Aimia’s 100%-owned synthetic-rope and netting business, a roll-up of two acquisitions made in 2023: Tufropes, an Indian synthetic-fiber rope and netting manufacturer serving aquaculture, maritime and industrial customers (bought March 2023 for CAD $249.6 million), and Cortland Industrial, a US-based designer and manufacturer of high-performance synthetic ropes, slings and tethers for aerospace, defense, marine, renewables and other heavy industrial end markets (bought July 2023 from Enerpac Tool Group for USD $26.6 million). Combined, Aimia paid approximately CAD $285 million for what it now reports as a single Cortland International segment. Operationally, the business is a niche industrial concentrated in marine/shipping rope, aquaculture netting (a quietly attractive structural-growth market), and specialty defense / aerospace tethers, which is the higher-multiple corner of the portfolio.

The operating reality has been tough. Q1 2026 revenue was CAD $32.7 million, down 19.7% year-over-year, with the decline traced to lower marine and shipping volumes, sales-order timing, and selling-price increases catalyzed by Middle East-driven raw-material cost rises. Q1 2026 adjusted EBITDA was CAD $4.5 million, a 13.8% margin. Annualizing the Q1 run-rate gives roughly CAD $18 million of EBITDA; the full-year 2025 figure was CAD $19.9 million.

As at December 31, 2025, Aimia’s goodwill related to the Cortland group of cash-generating units stood at CAD $42.5 million, after a CAD $14.0 million goodwill impairment. That impairment was the principal reason the consolidated business reported a CAD $9.9 million net loss for the period, and it was struck on a fair-value-less-costs-of-disposal calculation blending discounted future cash flow with a market-multiple approach. If the trajectory of revenue and EBITDA continues, it will be marked down again.

So what is Cortland actually worth on a private-market basis today? At a realistic specialty-industrial multiple of 6 to 8 times EBITDA on a run-rate of CAD $18–22 million, the implied enterprise value is roughly CAD $110 to $175 million. Even a generous strategic-buyer multiple of 9x on the high end of the run-rate gets you to ~CAD $200 million. Against the CAD $285 million Aimia paid, this is a permanent capital impairment of roughly CAD $85 to $175 million versus the original deal, which is a material chunk of the “wreckage of the old Aimia” narrative the new management has been quietly cleaning up. Critically, this gap is not yet fully reflected in book value. The CAD $42.5 million remaining goodwill plus tangible and other intangible Cortland assets - working capital, plant, customer relationships - sit on Aimia’s balance sheet materially north of a current private-market value. The CAD $3.66 reported book value per share carry Cortland at book, not at fair value to a strategic acquirer.

On the Q1 2026 call, management was explicit that there is “no rush“ to sell Cortland but that monetization would be considered “if an opportunity emerged that helped unlock value across the group.” Call it a high estimate, with maybe CAD $1.00–$1.50 of per-share air between book and a realized exit on Cortland. The thesis still works, because of the tax-loss optionality and the ability for Rhys to identify, then extract operational value, but it’s a reason why my stake in Aimia remains small relative to other investments.

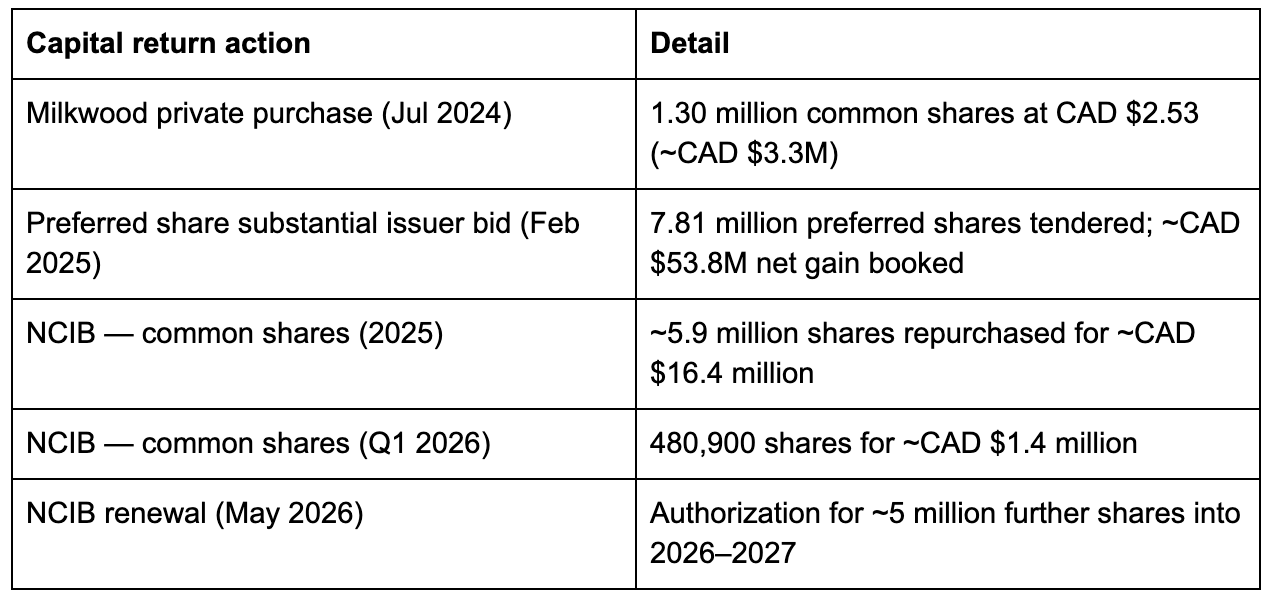

Capital Returns: Shrinking the Share Count

A management team’s treatment of its own shares tells you what it actually believes about value. Aimia’s recent record is consistent with a board that thinks the stock is cheap.

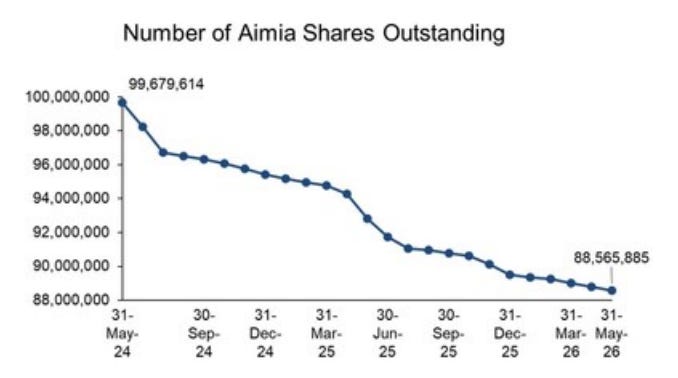

Note: I’ve used 89.4M shares outstanding in my valuation calculations since that was the number at the end of Q1.

The share count tells the story cleanly: roughly 99.7 million common shares outstanding in May 2024, ~91.1 million by July 2025, and now sits at ~88.6 million. That is over a 10% reduction in two years, executed at prices ($2.50–$2.90 range) that sit far below the CAD $3.66 book value.

The Investment Checklist:

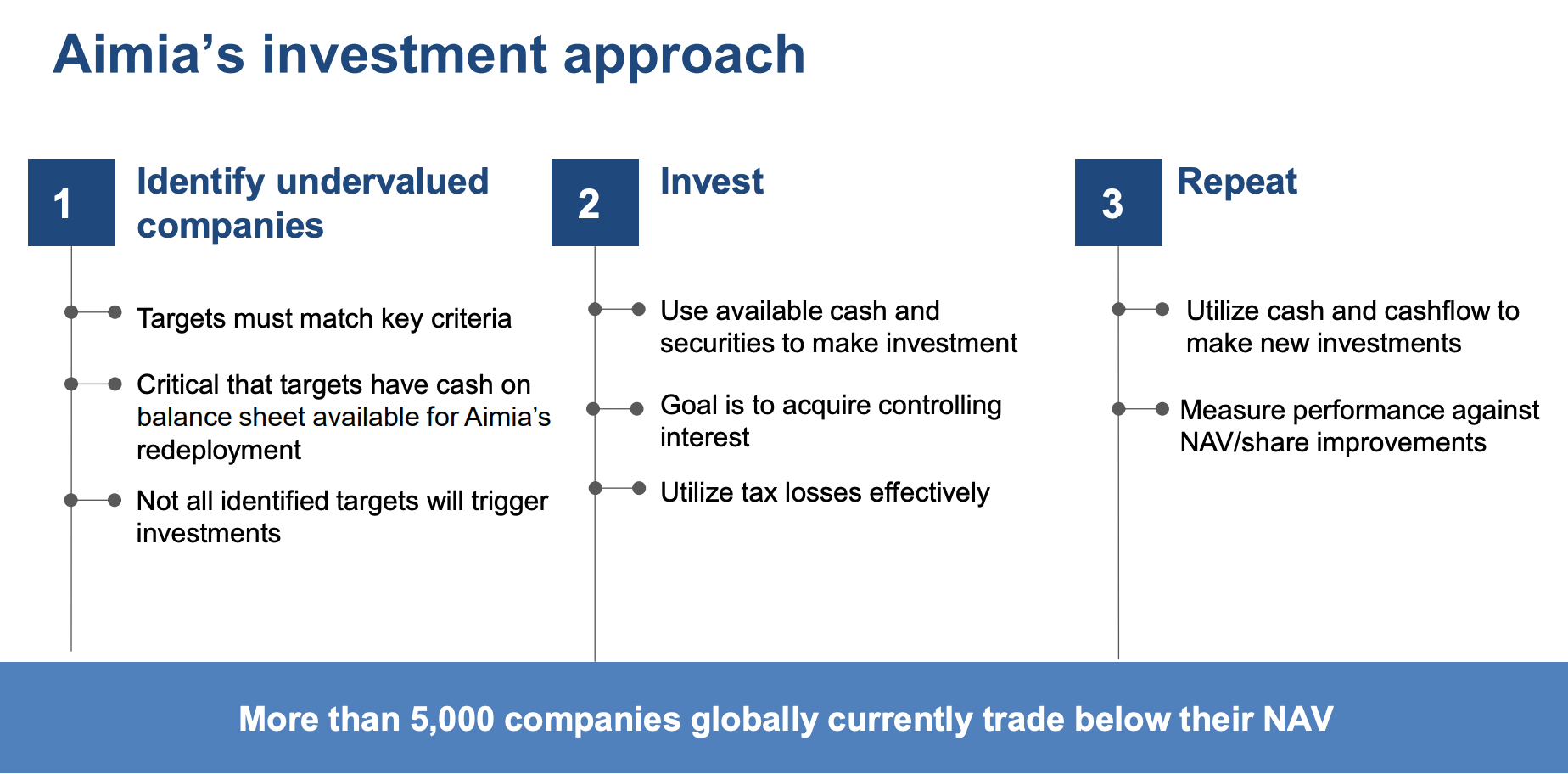

Management has been explicit about its criteria for investing their cash. Distilled from the Q1 2026 results, the Q1 2026 investor deck and the 2026 AGM presentation, Aimia’s checklist for a target investment is:

Undervalued versus intrinsic value: Management frames the universe as “more than 5,000 companies globally that trade below their NAV” and is fishing in that pond.

Cash on the balance sheet: This is stated as critical - targets should hold cash that Aimia can redeploy. The deck explicitly criticizes prior investments (Kognitiv, TRADE X) for having neither cash generation nor healthy cash balances. That mistake will not be repeated.

Genuine cash generation and profitability: The business must actually make money. No more story stocks.

Healthy balance sheets: Low leverage; financial resilience.

Controlling interests, not minority stakes: Aimia wants control to have the ability to direct capital allocation and route profits through the tax-loss structure.

Effective use of the tax-loss carryforwards: The ability to absorb Aimia’s losses in addition to their own.

Measured against NAV per share: Success is defined as growth in net asset value per share.

Management has also said the approach will be incremental, with capital deployed deal by deal, not in a single splashy transaction - and that it has already identified a short list of targets.

At its annual meeting, Aimia showed a slide titled “Sample target investments” - a table of five companies, identified only as Company 1 through Company 5, with their industry, market cap, net cash, forward EV/EBIT, forward FCF yield, and whether their tax losses are usable. The figures are in Canadian dollars. I have reverse-engineered each row from its financial fingerprint. Confidence ratings are mine alone and could be incorrect - especially considering the valuation assumptions are forward looking.

Who could Aimia buy? I own shares in two of these five companies

Reverse-Engineering Aimia’s Target Slide From the AGM: