Broadwind (BWEN, $2.52)

An inexpensive, U.S.-based industrial power micro-cap company.

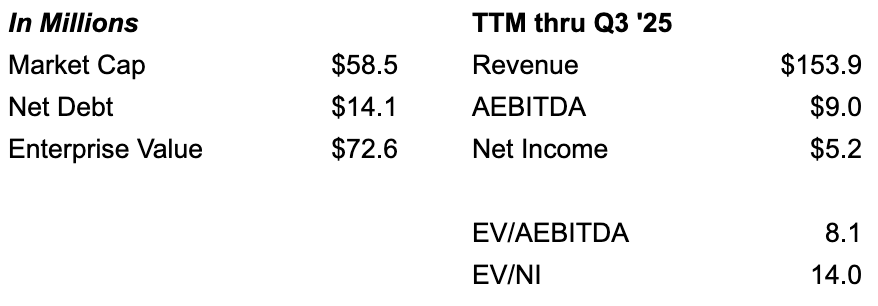

*Valuation figures are as of 11/24/25 close.

Based on my articles thus far, I’ve made it pretty obvious I love investments in power. This particular case is a small cap industrial component manufacturer, primarily to the power industry, that has recently bolstered its balance sheet through the exit of a heavy fabrication plant in Wisconsin. This enables them to bring most of that business to Texas and increase their business unit utilization.

While the share price is up over the past year, it has languished long-term due to inconsistent performance. After all, being a domestic industrial company, you would have expected a significant rise in price on the back of protectionism built to shield and grow our domestic manufacturing base. This is likely to bring inflation into the sector as capital flows adjust accordingly to reflect the improvement in unit economics -- if capital allocators view it to be sustainable. If the industrial buildout thesis plays out, it will give an advantage to any incumbents who will see the replacement value of their capital investments rise accordingly, but not reflected in their book value. This is partially why they were able to get an $8M+ gain on the sale of their Wisconsin assets.

Introducing, Broadwind.

Trading at 7.5 - 8.5x expected AEBITDA, I think Broadwind offers a compelling risk/reward in the near term.

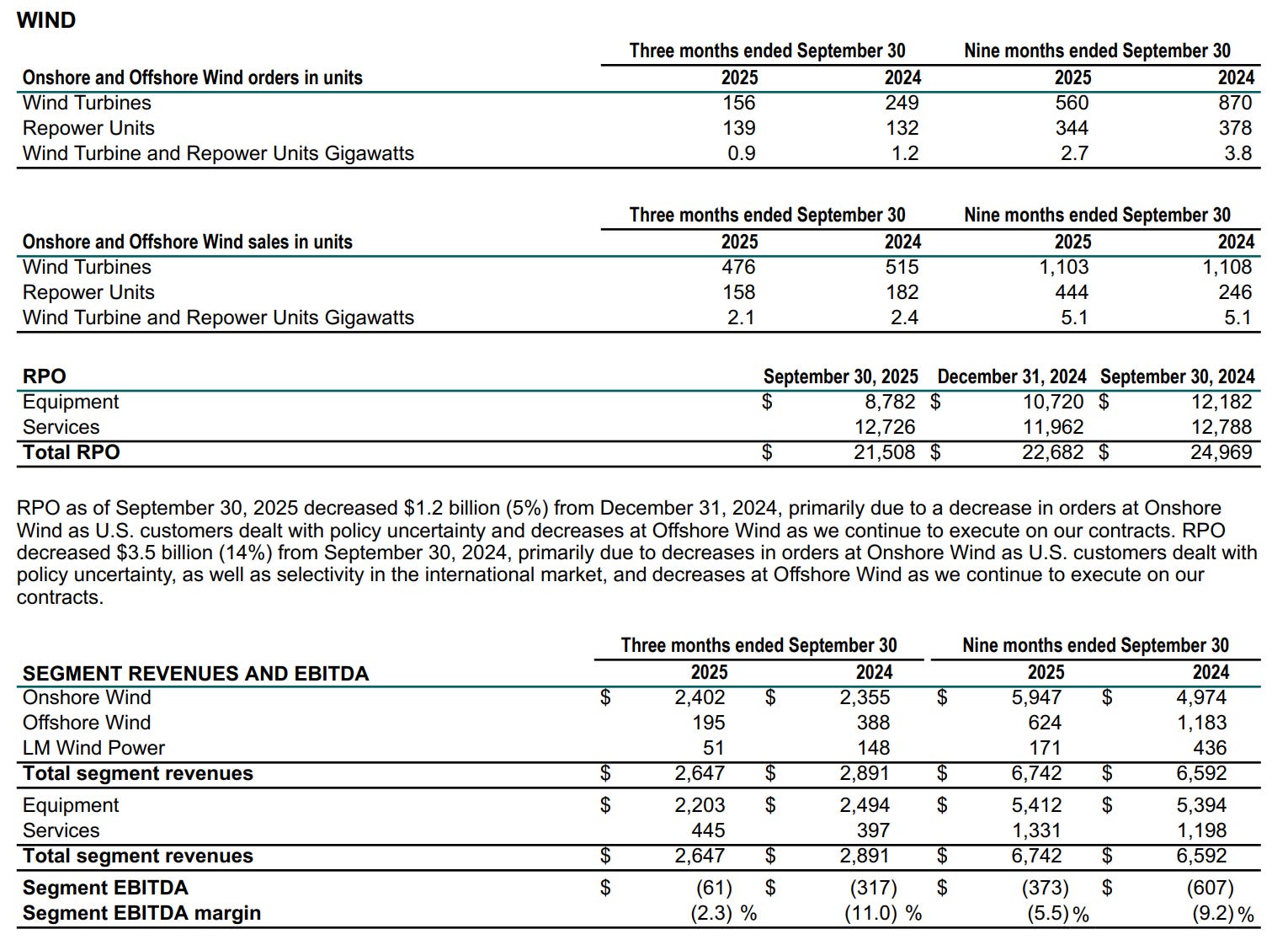

First, let’s get the negative out of the way. The majority of Broadwind’s revenue (54% YTD) is tied to wind power. Wind power and, more generally, renewables have been in the crosshairs of the Trump administration. This has introduced more uncertainty into their business model as tax credits are set to expire for wind projects that are not started by July 4, 2026 OR completed by December 31, 2027 (part of OBBBA). This not only impacts power installers/producers, it impacts domestic manufacturers through the Advanced Manufacturing Production (AMP) credits they receive.

Broadwind operates out of three divisions: Sequentially, Q2 -> Q3, each of these segments is showing promise with orders increasing over 100% / +90% YoY.

Heavy Fabrication: Wind towers, repowering adapters, natural gas pressure reducing systems.

Gearing: Custom gears, gearboxes and precision-machined components.

Industrial Solutions: Supply chain solutions, light fabrication, inventory management, kitting and assembly services, primarily serving the combined cycle natural gas turbine market.

I feel really good about Gearing and Industrial Solutions, especially considering their natural gas exposure and recent backlog wins (more on this later). The big question heading into 2026 is what their heavy fabrications division is going to do. Right now, backlog is well off this point last year, even with a recent $11M tower order in early Q4.

So what is the market missing?

Wind: Short-term (over the next ~12 months), I think a lot of wind demand will be brought forward to take advantage of the remaining lifespan of Inflation Reduction Act (IRA) tax credits. This gives immediate demand while allowing time to see how things shake out in the industry more broadly. With the long lead times across energy alternatives and the transient nature of American politics, my bet is that wind power is not going away. Furthermore, a significant portion of revenue is driven by repowering adapters, which are used to extend the life of existing turbines -- reducing a dependency on new builds. Regardless, the impact will be meaningful from a subsidy standpoint, as they currently get .03 per watt in AMP credits ($9.5M YTD ‘25). I expect some of this impact to be absorbed by tariff protections that give them pricing power versus foreign substitutes.

As stated by the Broadwind CEO in their Q3 call:

“In our heavy fabrication segment, we believe that domestic, onshore wind tower activity will continue at its present pace through 2026. We are encouraged by the continued momentum in the wind repowering market as we are seeing sustained demand from our OEM customers for the adapters we manufacture which are required to upgrade most legacy turbines. We have good visibility for tower production through 2026 and good customer indications beyond that.”

Natural Gas exposure: I think this is the under-appreciated component of Broadwind’s business. YTD through Q3 ‘25, ~20% of their revenue is coming from power gen. These are industrial components used in the construction of natural gas turbines. Examples of clients include GE Vernova. I do not expect this momentum to slow down any time soon as the incremental AI power demand is increasingly nat gas fed in the United States. GE Vernova has TTM revenue in this segment of $15B versus $84B (!) in firm backlog and slot reservations. Broadwind’s Gearing and Industrial solutions business units have backlog that is .82 and 1.34x trailing 12 month revenue, respectively. This is well above where they were last year.

NOLs of $290M+: While they have been getting tax credits for their wind manufacturing, they’ve been unable to utilize their net operating losses. As the Advanced Manufacturing Production (AMP) credits go away, they will be able to protect themselves from the tax man (hopefully they have something to protect!). Regardless, this could be particularly attractive to an acquirer within the significant guardrails that exist.

Property and capital investments (Price/Tangible BV is currently .9x): The $13M+ they recognized from their Wisconsin sale was for a leased property. Basically, they handed IES, a real compounder, (which gives me pause on 1) why they didn’t buy them in full 2) if Broadwind was the sucker at the poker table for this transaction) contracts, equipment and their leased footprint on the shores of Lake Michigan. I believe the market is assigning them too low a value for their other properties, especially those owned in TX and PA. Note: IES is not using the space for wind manufacturing.

Here is Broadwind’s remaining footprint:

I especially love their owned 175K sq. ft. facility in Abilene, TX. This has an incredible location in the middle of the AI gold rush. Furthermore, they should be able to get some operational benefit by moving some of their remaining heavy fab business from Wisconsin.

Let’s Talk Valuation

On a backward-looking basis we have a company trading at 8.2x their adjusted EBITDA. Valuing this company at a FCF multiple is most reasonable, however, that is very lumpy due to working capital volatility. Therefore, AEBITDA is a reasonable proxy because I do not expect the company to have significant CapEx requirements (2-3% of revenue).

Moving forward, I am excited to see what their Gearing and Industrial solutions businesses can do. Both have received a significant amount of orders and I think will begin to flex some operating leverage as they grow in the coming years. Gearing had a recent influx of orders that will take time to realize, so I expect that to be a better story from Q2 ‘26 onward.

Heavy fabrication is where past profitability and future question marks appear, a dangerous combination. Post Q3, they did announce a $11M wind tower project that will be executed over Q1’26, giving good visibility through March 2026. The company line thus far has been that demand is there. However, their wind clients (e.g. GE) have not been told what size turbines they’re purchasing, so the demand has not resulted in hard backlog.

I’ll be following along up to Q4 earnings to see if they book additional orders to get a sense of what 2026 performance will look like.

In summary

This is an inexpensive company. While wind is undoubtedly facing many headwinds due to the tax credit changes, power is not. There are multibillion-dollar datacenter installs situated near their plant in Texas that need to find power somewhere. The ability for GE, Siemens, Mitsubishi, etc. to deliver the needed nat gas capacity is going to be too little, too late. These datacenter operators are not going to allow their investment to go dormant and will need to get creative to operate. While wind is not the most attractive option in this landscape, it will be a necessary component to bridge the supply and demand mismatch that is already here.

Furthermore, you gain exposure to some very attractive facets of the business via their fast growing power generation sales (see, nat gas gearing and turbine components), a NOL shield and tangible assets (land, property & equipment) that are not appreciated by the market.

All this leads to a situation in which I think the most likely scenario is a sale of the company. Whether it’s through private equity or by way of a competitor, the push to reindustrialize the United States is here. Many capital allocators will realize it makes a lot more sense to buy versus build.

Next catalysts:

Based on their guide, they have indicated Q4 should be $2.2M - $3.2M in AEBITDA.

2026 forecast should be part of their Q4 call.

They have a $3M buyback in place. They also have a shelf registration active, which makes no sense to me. I’d love to see them buy back shares with the favorable terms of the $25M+ remaining LOC (sub 7%) they have.

Any new order announcements -- after Q3 close, they disclosed a $11M tower order.

There are those companies I monitor closely and others I’ll go for quarters without checking in (like my Favorite Compounder). This is a company where I sit down and turn up the volume on any earnings call. You need to be paying attention… which probably means I’m more of a tourist than true owner. However, for now, I believe the risk vs reward remains attractive.

What do I not Like?

Insider ownership is low. The only insider that has more than 1% ownership of the company is the CEO, Eric Blashford, with a ~2.7% stake.

Asset sale: The sale in Wisconsin signals the real pain Broadwind is expecting to face. While good it was done proactively and will hopefully shore up their utilization and margins, their capacity is significantly reduced. Their annual production capacity of towers is now 220 a year versus 550 with the Wisconsin property.

Government subsidies: Subsidies and tax breaks are a way for government to decide industry winners and losers. The benefits Broadwind receives are significant, with over $9.5M in YTD AMP credits. I expect/hope their ability to use NOLs & tariffs/anti-dumping provisions will make up some of this delta.

GE Vernova Wind Division Weakness: I pulled this from their Q3 report where you can see YTD orders are down 35% and 9% for wind turbines and repower units, respectively.

GE Vernova CEO, Scott Strazik

In Wind, the onshore volume trajectory remains too difficult to call. In the U.S., Onshore equipment orders remained soft as we shared in September. Customers still face permitting delays and tariff uncertainty that will likely weigh on our ‘26 Onshore revenue. We are closing deals with growing opportunities for services, repowering in the U.S. and new units in attractive international markets.

My Highlights from Broadwind’s Q3 Call

Eric Blashford - CEO

“Orders from our power generation customers more than doubled versus last year and now represent nearly 20% of revenue,” confirming a strategic shift in market exposure.

“Customer activity remains robust, with incoming orders rising to $44 million, up 90% year over year and doubling sequentially. Led by strong demand from power generation, increasing demand from oil and gas and industrial customers, combined with strong wind orders.”

“In 2025, margins were temporarily impacted by production process inefficiencies relating to a unique low volume tower build at our Manitowoc and Abilene facilities as well as lower capacity utilization levels within our Gearing segment. As production normalizes, we anticipate improved operating leverage through the duration of the year and into 2026. In the Industrial Solutions segment, we are investing in additional manufacturing capacity to address our growing backlog and meet future customer demand in the gas power generation equipment market.”

“Given the consolidation of our manufacturing base, we anticipate Broadwind, Inc. should be on pace to materially improve capacity utilization going forward.”

“In our heavy fabrication segment, we believe that domestic, onshore wind tower activity will continue at its present pace through 2026. We are encouraged by the continued momentum in the wind repowering market as we are seeing sustained demand from our OEM customers for the adapters we manufacture which are required to upgrade most legacy turbines. We have good visibility for tower production through 2026 and good customer indications beyond that.”

Thomas Ciccone - CFO

“Also boosting liquidity was a decrease in our operating working capital by almost $5 million, primarily driven by reduced inventory levels. We anticipate that working capital levels will decrease again during the fourth quarter.”

“Yeah. I think to answer your question about CapEx, we’ve made some investment this year. They’ve been relatively modest. We don’t expect anything that would move the needle from a consolidated perspective. As we look forward, historically, we’ve been about 2% to 3% of revenue as CapEx. We don’t anticipate exceeding that in ‘26 or Q4 or ‘26. But what I will tell you is we do intend to expand that plant into another portion of a larger building which we can get into. Increases our floor space by about 35%. Going into 2026. So that, along with the increase we’re making in staffing and equipment, we should be able to respond to this demand.”

“As a reminder, in 2024, the Manitowoc facility generated over $25 million of revenue, but adjusted EBITDA margin rate of approximately 8% to 9%. The majority of that 2024 revenue was industrial fabrication work that we do not anticipate replacing organically in 2025.”

“Regarding the capacity, we’re really only still about 45% full in gearing facility. So we have plenty of capacity to fill there as this business grows.”

Do your own due diligence. Any investment has the potential to fall to $0. I own shares in this company and am biased in their success. All information should be double checked, as it could be wrong.

I've exited ~50% of my position in the run-up for what I perceive to be better opportunities. I remain excited about their set-up potential in 2026.

Nice write-up, will include it in our next Best Stock Pitches letter.