Get $1 for $.28?

A government handout is ready to be harvested.

Not investment advice: First, read my full disclaimer here.

Special shoutout goes to Zack Wortman for reviewing and providing some input on my draft. He’s not investing full-time yet, but will be one to follow once he does.

While the Emergency Capital Investment Program (ECIP) has been a well covered investment angle, the current timing presents a very attractive entry point due to a catalyst expected to arrive in the coming months for certain recipients. This funding was used to prop up specific Minority Deposit Institutions (MDIs) in 2022 during a period of rising rates and struggling low-income consumers.

However, beware, not all the banks that received this capital are created equal. There are vast differences in the quality of these institutions and the timeline in which they have a path to turn the funds into equity.

This article is meant to do the work for you. After reading, you’ll have a better understanding:

How the ECIP redemption works

Who the highest quality (publicly traded) recipients were

When they have a chance to repurchase the funds to equity

How banks can use these funds to grow earnings once they don’t need to meet specific lending thresholds

The end result? Two banks I’ve added to my portfolio. They trade at a fraction of their ECIP-adjusted book value, generate reasonable returns on equity, and return capital to shareholders - with a path to unlock their ECIP funds in the next six months. Just as importantly, they are far overcapitalized and should be able to put their funds to work to grow earnings meaningfully. Speaking with their CEO and CFOs over the past week has furthered my conviction.

The Emergency Capital Investment Program (ECIP) presents an asymmetric setup. A government-engineered capital infusion where the economics overwhelmingly favor shareholders of a small handful of community banks. Of the 175 institutions that received ECIP funds, I’ll provide a breakdown of the public companies according to the important questions to ask:

1) Materiality: For which banks will this have a material impact?

2) Quality: Which of these institutions are the highest quality?

3) Timeline: How quickly are they likely to buy back their preferreds?

4) Earnings: How overcapitalized are they? What could it mean for earnings growth?

The confluence of those four factors led me to the investments I made.

Materiality: For which banks will this be a material impact?

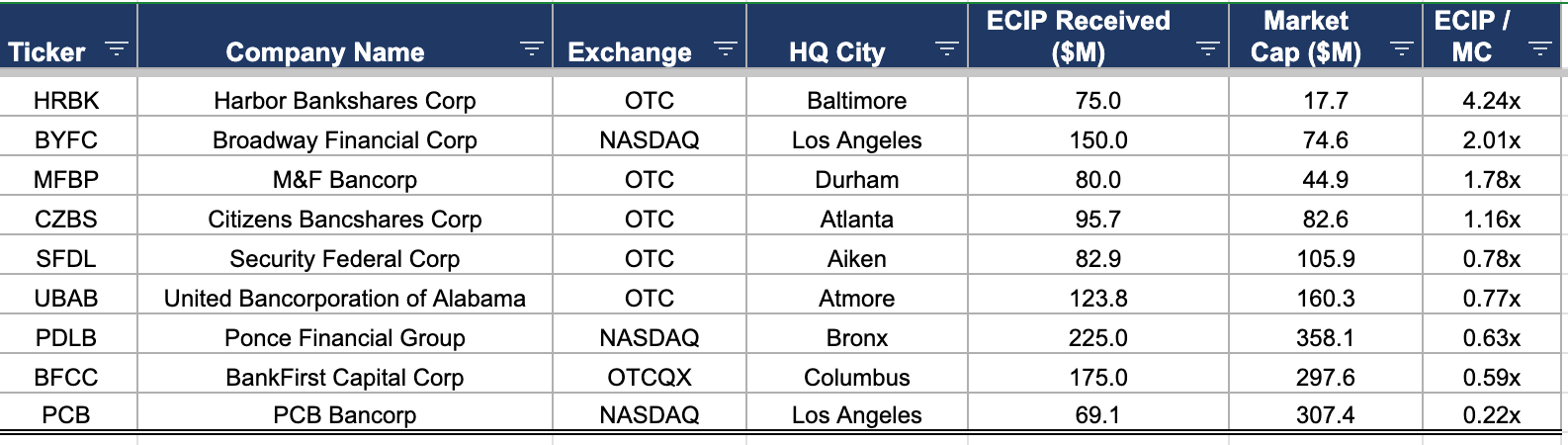

For the public recipients, there is a wide variance how accretive buying their preferreds from the treasury are likely to be. As measured based on their market cap, the amount of ECIP funding received ranges from .2x - 4.2x (!). If that were the only factor, we’d be taking a trip to Baltimore.

Sorted from highest to lowest ECIP funds / MC

Quality: Which of these institutions are the highest quality?

Now that we are almost five years into the funds being granted, it gives us a body of work from which to assess how well management teams have put their ECIP windfalls to work. The variances are drastic.

This program gave funds to banks indiscriminately, regardless to if they had any demonstrated ability how to lend. Those that didn’t know what they were doing before certainly weren’t going to figure it out with these windfall funds. The government would have been better off flushing some of these dollars down a drain than giving these institutions the incentive to line their pockets or throw them away in their respective communities.