Let's Take a Step Back

Big Picture First: Markets, Policy, and Positioning

Periodically, I plan on making free-form posts that will collect my thoughts, watchlist ideas, and recent investment actions.

To be a good investor, you need to have a rational understanding of how the world works. Not how you want it to work. How it actually works.

Therefore, I disagree with investing pundits who advocate ignoring the macro picture. Don’t miss the forest for the trees. Is there a higher likelihood you will be wrong? Absolutely, there are so many complex variables at play. However, successful institutional investors don’t sit down and start hammering away at which investments to make - they start with the big picture, first.

As we sit here at the end of January, it has been a fascinating few months. Valuations look increasingly untethered from fundamentals. Geopolitical tensions continue to simmer. And the metals trade has been strong enough to bring a smile to the dour gold-bug cohort. The thing I appreciate about age is it gives you perspective. Perspective to process, but not get too caught up in the day-to-day happenings.

I don’t try to predict where interest rates will be by year-end; I try to map out what I think has a high probability of happening over a long horizon. Let me see how wrong I can be.

Here are a couple of observations:

Global Fiscal Policy: Governments have been spending like lunatics for some time now. This became a big issue in the wake of COVID and has never returned to sane levels. Currently, I do not foresee a world in which spending is reined in to be in line with tax revenue or even GDP growth. We’ve come to expect a lot of money printing from Central Banks. Expect a lot more moving forward. The last page in the Economist brings this home for me every time. I wish corporate or personal balance sheets were better. (This IMF report does a pretty good job summarizing)

The new Red Sea, government budgets

Is this BlackRock BDC losing 19% of its net asset value a canary in the coal mine?

Monetary Policy: For this, I will speak from the perspective of a U.S.-based investor. Our administration seems determined to low rates regardless of the second-order consequences. Through fear, intimidation and an upcoming opportunity to name the Fed successor, it seems to be a matter of ‘how much’ rates will decrease. Here is a good interview with the current prediction market favorite to be the next Chair, Rick Rieder.

Trade Policy: Tariffs were not on my radar two years ago. Now we are in a situation where the trade-weighted average effective tariff rate is ~15-20%. Unfortunately, they are constantly changing. This unsettles capital and makes it very difficult to make large capital outlays when the economics underpinning them (e.g. to build out domestic manufacturing) are constantly altered.

Foreign Policy: To layer on top of the tariff situation, U.S. foreign policy has been unpredictable, bellicose and arrogant. This has alienated adversaries and long-term allies alike. The United States is now squarely on an island. On the flip side, it should pull the rest of the world closer together. Canada getting closer to China. Europe reaching a free trade agreement with India. These agreements will become a weekly thing.

“Trust is the easiest thing in the world to lose, and the hardest thing in the world to get back.” — R. M. Williams

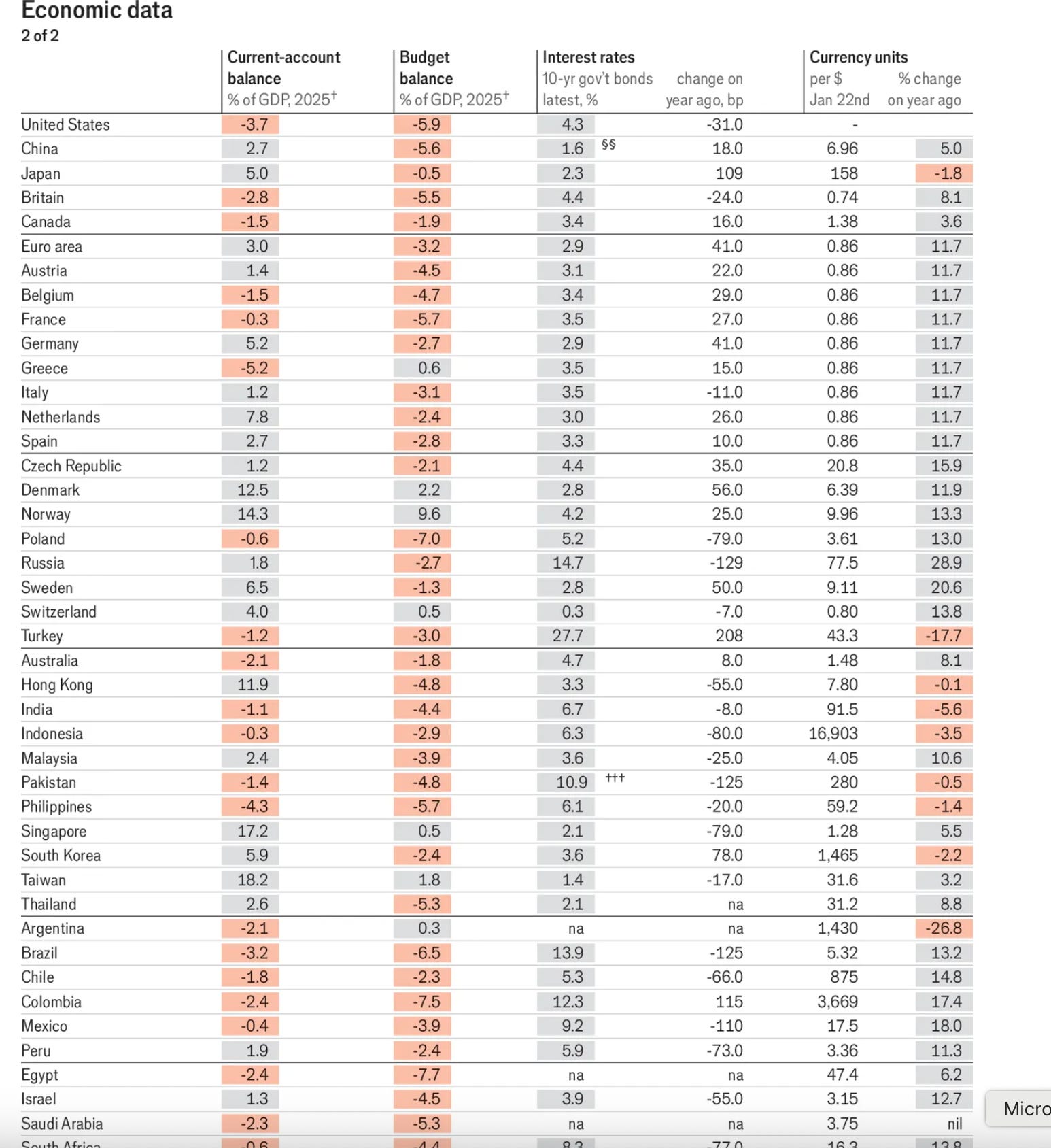

As it pertains to the United States of America, we are now in a situation where the world distrusts us. With that, it becomes less likely the international community continues funding the largesse we have been living off of for the last 40 years via huge current account and fiscal deficits. See, when you are the reserve currency, you are given certain privileges. You have more borrowing power, larger credit leeway and create currency demand serving as the preferred payment method for certain assets and inter-country transfers. What happens now that trust is gone? We are only beginning to understand the repercussions, but I do not think we’ll be seeing a stronger dollar anytime soon. Bond yields are not particularly promising, either. Over the past year, the 10-year is down only ~30 basis points (bps) vs a 75 bps decline in the Fed rate. I believe this is the beginning of foreign governments taking their net import surplus and hoarding the likes of gold, shunning Treasuries.

Where does this all point? Inflation. Buckle up.

Financial Valuations: While I do not know what inning we are in, I’m pretty certain we’ve turned it over to the bullpen. Valuations are high and expectations are higher.

I like this website where you can filter by a country’s P/E and standard deviation to historical prices. It is concerning that only one country is below its 200-day average trading price (India) and the vast majority are multiple standard deviations above average 20-year valuations.

Forget buy low and sell high. This is the buy high and try to sell higher.

Thanks for the uplifting news! What can I do? First off, I’m not calling this a ‘top.’ I have no idea what is going to happen in the near future. However, I do think it behooves one to be proactive and figure out how to protect yourself. Beta trades are fantastic in an up market. Even better if they are combined with margin. Be careful where you’re positioned on the risk spectrum for when the tide turns.

Everyone needs to play their own game. The one I’m playing is focused primarily outside the United States. Investing in small/mid-sized companies with strong balance sheets, decent growth prospects that trade at low valuations.

On a Positive Note

There has never been a better time to follow incredible up-and-coming investors. Between X, Substack and niche communities like MicroCapClub, the global talent pool is staggering. It is an incredible time to be young, hungry and AI native. Here are a couple of my favorites:

Kreuzmann’s Ideas: Strong hit rate. I think his thesis of going A-Z through markets to unearth gems is the right approach.

Simeon Capital: Strikes me as being a very strong networker who gets after it.

Value Hunt: He’s taken over a lot of the content responsibilities at MicroCapClub and is killing it with his investor and company interviews.

It’s also just necessary to include a16z because I learn something from every article they publish.

Q1 2026 Watchlist

Gravity (GRVY): South Korean gaming company. Trades close to cash, MC/E of ~7x, great margins, expect strong near-term growth on recent game releases. The catalyst: Majority investor GungHo (publicly traded in JPN) has been under pressure from a local activist (Strategic Capital), this has resulted in their CEO getting replaced. Fun fact: The founder of GungHo is Masayoshi Son’s little brother.

I-Tech (ITECH.ST): Great (company-funded) write-up can be found here. Interesting entry point with them down over 50% from previous highs. There are multiple value propositions. The main one: It allows large boats to minimize drag and conserve fuel. The problem? The incentives are all messed up. Ship owners pay for the vessels and their upkeep, but then pass them to operators. Therefore, why would they incur a higher price without accruing the rewards? Now that copper has rallied and copper-based paints are their primary competitor, it may be a good entry point.

Matrix Composites (MCE.AX): Supplier of subsea buoyancy products for O&G companies (may have long-term offshore wind tower application as well). If you’ve read any value investor blogs over the last 18 months, they probably have some offshore rig post in there. If production is to increase, offshore is the place where supply can be increased at a reasonable marginal cost. Matrix owns a great manufacturing plant in Western Australia and should be a key beneficiary. I’d be surprised if I do not own shares at some point in 2026.

Zicom (ZGL.AX): Singaporean heavy industry company that thinks about things in the right way. I loved the note from the Chairman. Company is cheap at 5-6x earnings. “Our greatest glory is not in never falling, but in rising every time we fall.” - Confucius (551-479 BC)

Sofwave (SOFW.TA): Aesthetic skin tightening and rejuvenation device manufacturer that is less invasive than their competition. It’s a razor blade model where they earn a royalty per pulse. Now with a strong install base, they’ve inflected to profitability and should continue their strong growth and margin expansion. I made the mistake of selling them far too early and buying their deep value (trap) peer, InMode, who is a rumored takeout target.

Marpai (MRAI): Insurance TPA recently announced the departure of their President, Dallas Scrip. This comes on the previous departure of their top salesman, John Powers. When I talked to Damien Lamendola (CEO) in April 2025, he was pounding the table about the opportunity Marpai had in front of it. I view the departures as negative indicators, but will take a close look at the next two quarterly reports. 70%+ of health plan renewals happen January 1, so Q1 earnings should be sticky throughout the year.

General Enterprise (CITR): Company has an eco-friendly fire protection solution. Three ways to commercialize: home based sprinkler systems, treated wood and fire prevention. At $130M valuation, the market thinks they have something. 2026 will be a telling year - it’s time to sell.

As things develop, I will be adding color to the subscriber chat.

Investment Actions – Buys and Sells

Does not include the three illiquid companies that will be upcoming write-ups. They are domiciled in Australia, South Africa and Norway - falling squarely in the deep value category:

What I’m buying: Including a gold miner I’ve been adding to at 2x my expected 2026 earnings.