Pharos Energy

A stock that could earn their EV in less than two years at $90 Brent.

Not investment advice: First, read my full disclaimer here.

*Numbers are in USD (reporting currency) unless otherwise denoted.

MC: $150M EV: $110M // TTM: Revenue: $114M FCF: $30.5M // EV / FCF = 3.6x

Pharos is one of those names that slides past most screens. It’s a ~£116M market cap oil producer listed on the London Stock Exchange, operating in Vietnam and Egypt - two jurisdictions that don’t inspire a lot of “institutional comfort.” Furthermore, the P&L covers up the cash generating strength of the underlying business.

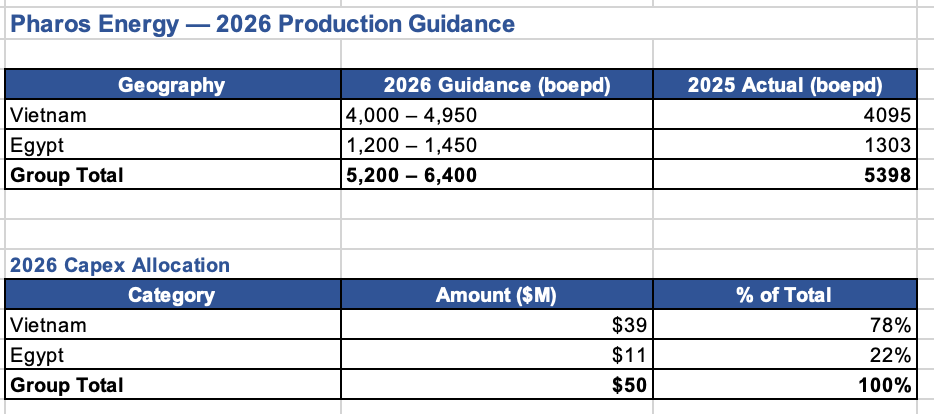

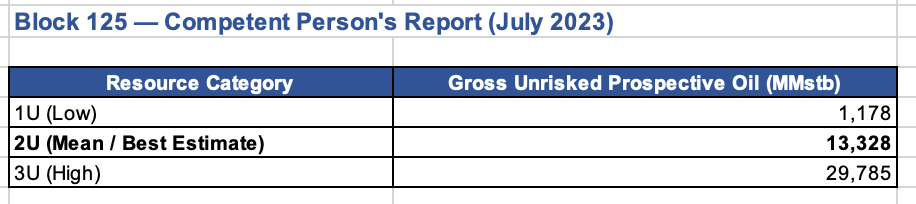

Here’s the setup: Pharos ended 2025 with $40.2 million in net cash on a debt-free balance sheet. 2026 production guidance is 5,200-6,400 boepd, up +7% at the mid-point from approximately 5,400 in 2025. Vietnam is expected to carry the growth through a six-well drilling program targeting a ~20% production uplift weighted toward the second half of the year. The Vietnamese crude (~80% of production) sells at a $5-6 per barrel premium to Brent into the domestic market. Egypt was expanded to a 20-year concession with improved fiscal terms. And then there are Blocks 125 and 126 - two frontier exploration blocks in Vietnam’s Phu Khanh Basin where a 2023 Competent Person’s Report identified a mean unrisked prospective resource of 13.3 billion stock tank barrels.

The enterprise value is approximately $110 million. The company has no debt. It’s run by CEO Katherine Roe and CFO Sue Rivett - who together bring decades of E&P and capital markets experience. It pays a dividend and hedges only 24% of production in ‘26, so is positioned to capture great upside tied to spot.

Let me walk through why I think the market is wrong on this one.

The Business: Two Countries, One Cash Engine

Pharos Energy is a London-listed independent oil and gas company with producing assets in Vietnam and Egypt, plus frontier exploration acreage in the Phu Khanh Basin offshore Vietnam.

Vietnam (~80% of production): Pharos holds interests in two producing blocks in the Cuu Long Basin - one of Southeast Asia’s most prolific hydrocarbon provinces. Block 16-1 contains the TGT (Te Giac Trang) field, where Pharos holds a 30.5% working interest, and Block 9-2 contains the CNV (Ca Ngu Vang) field, where Pharos holds a 25% working interest. These are shallow-water, low-cost, well-established assets tied to existing infrastructure. Combined Vietnam production ran at approximately 4,095 net in 2025.

The critical feature of the Vietnamese crude: it sells at a premium to Brent. This is not a typical discount crude. TGT oil has historically commanded a $5-6/bbl premium to Brent in the domestic Vietnamese market, driven by local refining demand, crude quality, and Southeast Asian supply-demand dynamics. When most E&P investors are accustomed to discounts - WCS to WTI, Oman to Brent - a premium is a differentiator that feeds directly into realized revenue per barrel. This production is sold into Vietnam for domestic use (VN is a net oil importer) and they’ve not had any significant payment issues/disputes over their operating partnership.

Egypt (~20% of production): Pharos holds a 45% non-operating working interest in the El Fayum concession in Egypt’s Western Desert. The operator is IPR Lake Qarun Petroleum (55%), an Egyptian-American firm (HQ’d in Irving, TX) that took over operatorship following Pharos’s farm-out in 2022. Egypt contributed 1,303 bopd in ‘25. These are low-cost, shallow, onshore wells - operationally simple but requiring a steady diet of new wells to maintain/grow production. Management is bullish on Egypt: the goal is to double production volumes over time, and the recently approved consolidated concession agreement comes with meaningfully improved fiscal terms that revert back to October ‘25 (approval is expected later in ‘26).

Blocks 125 & 126 (Exploration): Pharos holds a 70% operated interest in two frontier exploration blocks in the Phu Khanh Basin, a relatively unexplored deep-water basin northeast of the producing Cuu Long Basin. The exploration period has been extended through November 2027. I’ll come back to these in the growth section, because the resource potential is extraordinary relative to the company’s current market cap.

The Numbers: What You’re Buying

MC: $150M EV: $110M // TTM: Revenue: $114M FCF: $30.5M // EV / FCF = 3.6x

Let me highlight a few things.

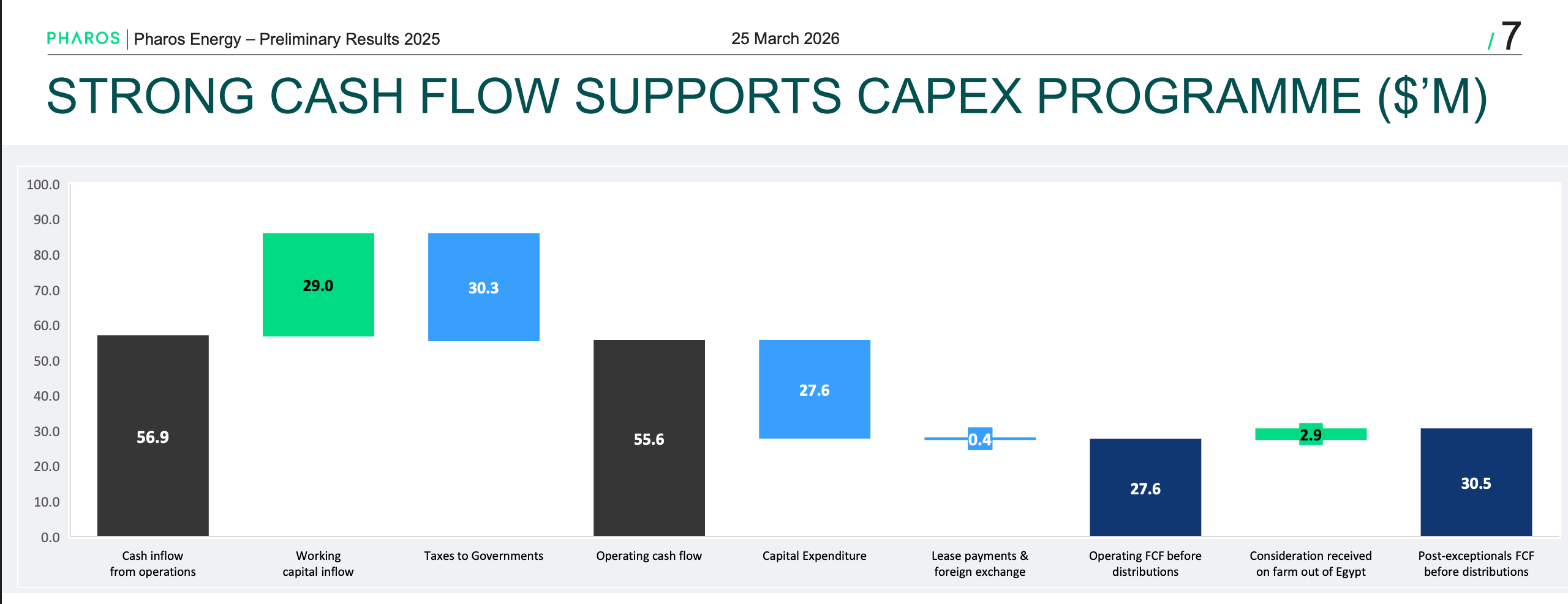

Cash build: Pharos went from $16.5M at year-end 2024 to $40.2M at year-end 2025. That’s a $23.7M swing, driven primarily by the $20M payment from Egypt. The company has zero debt, you’re getting about a quarter of your price in cash.

Revenue declined, but that’s context-dependent: The drop from $136.1M to $114.6M reflects lower commodity prices and the natural decline of the producing base before the 2025/2026 drilling program kicks in. The six-well campaign in Vietnam - four wells in TGT and two in CNV - is the bridge between the current decline and the production uplift that management is targeting.

The EV/boe gap: At an enterprise value of ~$110M and post-consolidation 2P reserves of approximately 17-19 MMboe, the market is pricing Pharos at ~$6-7 per barrel of oil equivalent. The book value - the carrying amount tested against a value-in-use DCF of the 2P reserve profile equaling ~$270M using what I perceive to be conservative assumptions. That is a wide gap. Either the market is right that recoverable reserves are overstated, or the stock is materially undervalued on a reserve basis.

Growth: The Vietnam Drilling Program and What Comes After

The near-term growth story is straightforward: Pharos is in the middle of a six-well drilling program across the producing TGT and CNV that is expected to complete by H2 2026. The program targets a ~20% production uplift from current Vietnam levels. This would take net Vietnam production from approximately 4,000 boepd to potentially 4,950 boepd at the upper end of 2026 guidance.

2026 guidance increased from 2025 levels:

The capex to fund this is $50 million - up sharply from $27.6M in 2025. That’s a significant year-over-year ramp. Of the $50M, $39M is allocated to Vietnam (the tail end of the six-well campaign plus facility work) and $11M to Egypt.

But the real growth optionality that could make this an asymmetric position sits in the Phu Khanh Basin.

Blocks 125 and 126: The Frontier Exploration Upside

Pharos holds a 70% operated interest in Blocks 125 and 126, located in the Phu Khanh Basin offshore central Vietnam. The basin sits northeast of the proven Cuu Long Basin and remains relatively unexplored - a frontier play in a country with an established offshore hydrocarbon industry.

In July 2023, Pharos released a Competent Person’s Report on Block 125. The numbers are staggering:

Thirteen billion barrels at the mean estimate. Even at the low end, 1.2 billion barrels. These are unrisked, prospective resources - meaning they are geologically estimated volumes that have not been confirmed by drilling and are subject to exploration risk, geological chance of success, and commercial viability. They are emphatically not reserves. But the scale of the resource potential relative to Pharos’s $100M enterprise value is worth sitting with for a moment.

The technical profile is encouraging. 3D seismic processing is complete and interpretation has revealed greater opportunity in the deeper water sections of Block 125. Multiple world-class prospects have been identified. The company is actively seeking farm-in partners to share the cost and risk of a commitment well - which would be the first real test of the basin’s hydrocarbon potential in this area. The cost and technical nature of this basin exceeds their currently producing assets in the country. With well costs that could exceed $50M, it’s likely any partner would be an oil major. To be clear, this will take a long time to develop and get to first oil.

The exploration period was extended by two years in 2023 and now runs through November 8, 2027. Management indicated at investor presentations that an update on the exploration program - including farm-in partner discussions and rig contracting - was expected in the coming months. This could be the catalyst for a big value unlock.

Here’s how I think about it: Blocks 125 and 126 are worth zero in my base case valuation. They are pre-drill, frontier exploration with no guaranteed outcome. But the optionality is enormous. If a farm-in partner takes a meaningful stake and funds a commitment well, the market will be forced to assign some probability-weighted value to the resource. Even a 1-2% geological chance of success applied to 13.3 billion barrels of mean resource, at any reasonable risked barrel value, starts to move the needle on a $100M EV company.

This is the kind of embedded option that the market systematically undervalues in small-cap E&Ps and it’s a core reason why I think Pharos is more interesting than it looks on the surface.

Egypt: Improved Economics and a 20-Year Runway

The Egypt story is about longevity and improving terms, not about near-term production growth.

Pharos farmed out 55% of its Egyptian assets and operatorship to IPR Lake Qarun in March 2022. The deal structure was well-designed: $5M cash at completion, $38.4M in carried costs (IPR funding Pharos’s share of future development). Pharos received a significant working capital boost in Egypt over 2025 - with their AR dropping from $29.5M to $7.4M over the course of the year. In my call, they mentioned an expectation to receive the outstanding $6M Egyptian receivable balance by the end of Q2 ‘26.

The more important development is the consolidated concession agreement approved by EGPC’s Executive Board. This combines the El Fayum and North Beni Suef concessions under a single framework with improved fiscal terms. Higher cost oil recovery and an increased profit oil will result in more cash per barrel produced, even at the same production levels.

The 20-year development lease and up to 30-year exploration terms on three new areas (West Silah, Beba, South Wadi El Rayan) give Egypt a long runway. The consolidation also enables the upgrade of approximately 3.1 MMboe from 2C contingent resources to 2P reserves - a 25% uplift net to Pharos’s interest - pending Parliamentary ratification expected in 2026.

Egypt is not the growth driver. It’s the ballast: a long-life, low-cost producing asset with improving economics that provides base-level cash flow and reserve support.

Management:

Katherine Roe became CEO in 2024 after successfully running Wentworth Resources as CEO from 2019, ultimately negotiating its sale to Maurel et Prom (another company I own) in December 2023. Before that, she spent 11 years heading the Natural Resources team at Panmure Gordon. She knows how to run a small-cap E&P, she knows how to talk to the market, and she has experience across emerging and developing market jurisdictions - exactly the skill set required for a company operating in Vietnam and Egypt.

Sue Rivett serves as CFO and has been with Pharos for over five years. Her background spans senior finance roles at Conoco, ARCO British, JKX Oil & Gas, and Seven Energy. She has deep experience with JV structures, M&A, and the full range of FTSE finance functions.

Both have recently increased their personal shareholdings, but do not own a meaningful amount of the company.

The capital allocation framework is ok. I’d like to see more shares purchased: a dividend floor of no less than 10% of operating cash flow (increased 10% year-over-year), a completed share buyback program that repurchased 30.7 million shares at an average of 23.65p, and a willingness to keep $40M+ in net cash on the balance sheet as a buffer. Management maintains a limited hedging position with only 24% of 2026 volumes hedged, providing a path to capture spot upside/downside. With no debt and no reserve-based lending facility requiring minimum hedge ratios, they can afford to make that choice.

Risks

The risk profile is what keeps this stock cheap, and investors need to understand what they’re underwriting.

1. Vietnamese Working Interest Depreciation and License Expiry — The Central Risk

Pharos’s Vietnamese assets operate under Production Sharing Contracts with the Vietnamese government. These contracts have fixed terms, and critically, the working interests step down at defined dates before the licenses ultimately expire.

Block 16-1 (TGT field):

Current working interest: 30.5%

Effective December 8, 2026: Working interest steps down to 25.33%

License runs through approximately 2031/2032

Block 9-2 (CNV field):

Current working interest: 25%

Effective December 16, 2027: Working interest steps down to 20%

License runs through approximately 2032

On December 8, 2026, Pharos’s TGT working interest drops by 5.17 percentage points overnight. That is a ~17% reduction in the company’s entitlement to production from its largest field, effective roughly nine months from now. The CNV step-down follows 12 months later.

If TGT is producing 3,500 boepd net to Pharos at a 30.5% working interest, a reduction to 25.33% means net production drops to approximately 2,903 boepd - a loss of ~597 boepd. At $80 Brent, that’s roughly $19.6M in annual revenue that evaporates from the contractual step-down.

The license expiry dates of 2031/2032 are further out, but they define the ultimate life of the producing assets. After expiry, the fields revert to the Vietnamese government. There is no guarantee of further extension. Vietnam has historically renewed PSCs on a rolling basis, which explains the pattern of year-to-year extensions that can look uncertain from the outside. But the government’s willingness to extend is driven by its own domestic energy needs, the quality of the operating partnerships, and the commercial viability of continued production. It is not automatic.

The combination of near-term working interest erosion and medium-term license expiry is why the market prices Pharos’s Vietnamese reserves at a steep discount. It is also why management is investing $39M in Vietnam capex for 2026 - to maximise production and cash flow extraction from these assets while the working interests are highest.

Furthermore, the recently extended Blocks 125 and 126 is only for a two year term.

2. M&A

Pharos is well aware they are a small fish in a big pond. Being a sub-scale producer that holds working interests in regions with significant jurisdictional risk has not been the road to riches for many. However, I think if they focus on operating, organic growth and buybacks, it is the best path to unlock shareholder value.

3. Egyptian Execution Risk

Egypt is operated by IPR Lake Qarun, not Pharos. Pharos is a 45% non-operator — meaning it has limited control over the pace and quality of development drilling. If IPR underperforms operationally, Pharos bears the consequences pro rata. The goal of doubling Egyptian production is ambitious for a set of shallow Western Desert wells that require continuous drilling to offset decline rates.

4. Natural Decline Rates

Oil fields decline naturally. Neither Pharos nor its operator has published explicit decline rate assumptions for TGT, CNV, or El Fayum in a way that allows outside investors to model the production trajectory with precision. The need for a six-well drilling program just to grow production by ~20% implies that underlying decline rates are meaningful. Potentially 15-25% per annum for mature fields of this type. Without continuous investment, these assets bleed production.

Why is this company so inexpensive? It has been a melting ice cube. Here is the production profile over the past decade.

5. Exploration Risk on Blocks 125 and 126

The 13.3 billion barrel mean prospective resource is geologically estimated and completely undrilled. Frontier deep-water exploration in a relatively untested basin carries significant geological risk. The probability of commercial success on any single exploration well is typically 10-25% in frontier basins. Pharos needs a farm-in partner to fund the commitment well. If no partner materializes before the November 2027 deadline, the blocks may be relinquished.

6. Jurisdiction Risk

Vietnam and Egypt both carry country risk. Vietnam’s regulatory framework for foreign oil companies has been stable but is ultimately subject to government discretion. Egypt has a history of delayed payments (the EGPC receivable that took years to resolve) and regulatory unpredictability. Furthermore, the tax policies in both regions is extremely punitive, with close to 50% tax rates. An easy (and popular) mechanism would be to continue to push this north as barrel prices increase.

Valuation: What the Market Is Missing

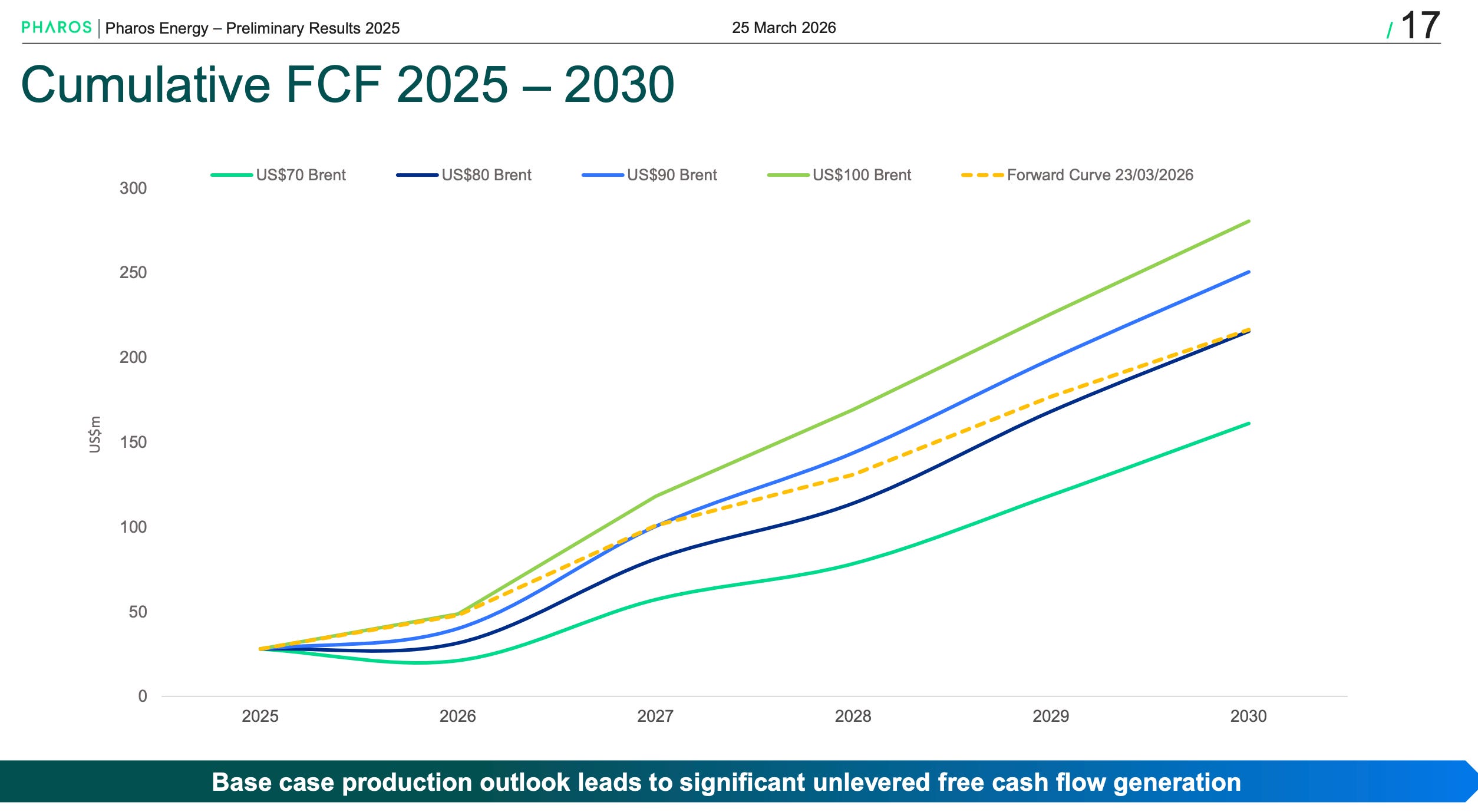

This is my favorite chart from a straight to the point investor deck Pharos released with prelim earnings. While speaking with management, they called this the ‘sweat the asset case.’ Yes, investment will be higher in 2026. After that, you can see a step change improvement in the slope of the line. The net? If able to execute and Brent stays at $90, you get your EV out in 21 months (by the end of ‘27). What happens if it goes back down to $70, which futures remain well above? We have to wait until 2029 with a few more years of contracted Vietnamese supply still to go.

That’s a situation where I feel pretty good on getting full EV value within the next 2-4 years while holding a lottery ticket for the unexplored blocks that hold great potential.

If not achieved, I will expect it to be due to accretive growth opportunities that have a strong ROI.

The valuation case rests on the gap between what the market is pricing (~$6-7/boe on 2P reserves) and what the IFRS-tested book value implies is recoverable (~$15/boe). That’s a roughly 60% discount to carrying value.

What to Watch

The Vietnam drilling program results. The final infill well on the H4 fault block reached total depth in March 2026 and is expected online in April. Production outcomes from this well and the remaining appraisal wells will determine whether the ~20% uplift target is achievable.

Blocks 125/126 farm-in update. Management guided for an update on farm-in partner discussions and rig contracting by the midpoint of the year. This is the single highest-asymmetry catalyst in the thesis.

TGT working interest step-down (December 8, 2026). This is a known event — but the market’s reaction to the actual production impact will be informative. Watch Q1 2027 production figures closely.

Egyptian concession ratification. Parliamentary approval of the consolidated concession would formalize the improved fiscal terms and upgrade 3.1 MMboe from 2C to 2P reserves.

Oil prices. With 76% of production unhedged in ‘26, Pharos is a leveraged bet on Brent. The $5-6 premium in Vietnam amplifies the upside but doesn’t protect the downside.

Capital allocation decisions. Whether management maintains the dividend growth trajectory, initiates a new buyback, or deploys cash toward a new asset acquisition will signal their confidence in the forward outlook.

Conclusion

Pharos Energy is priced for run-off. The market sees a small-cap E&P with declining Vietnamese working interests, limited analyst coverage, and jurisdiction risk. It assigns a valuation that implies the assets are worth significantly less than book value. I think that’s wrong.

What I see is a debt-free company with $40M in net cash, producing assets that sell crude at a premium to Brent, improved 20-year concession terms in Egypt, a drilling program targeting 20% near-term production growth in Vietnam, and 13.3 billion barrels of mean unrisked prospective resources in a pair of frontier exploration blocks that the market isn’t valuing.

The risks are real. The Vietnamese working interest step-downs - 30.5% to 25.33% in December 2026 on TGT, 25% to 20% in December 2027 on CNV - are contractual certainties that will erode the production entitlement even as gross field production holds steady. The licenses expire in 2031/2032, giving the producing assets roughly six years of remaining life. These are not forever assets. But at $6-7/boe, I don’t think the market is correctly pricing the cash flow these assets will generate over their remaining lives, let alone the exploration optionality or the improving Egyptian economics.

The management team is aligned, conservative on the balance sheet, and making sensible capital allocation decisions. The 24% hedge ratio is a conscious bet on oil prices that allows them to take advantage of the current situation in the Middle East. Unless there is a geopolitical shock to the system (heavy taxation, expropriation, war where assets are located, etc), I think there is a good probability one of two scenarios occur in the next 2-4 years:

Generate cash equal or above EV.

A clear path to sustainable growth with much of the CapEx burden shouldered by an operating partner.

Katherine and Sue have a history of being conservative and focused on ROI. They have not chased growth, a trap many oil companies their size fall into. As long as that focus does not change, I am excited about the future prospects for Pharos.

Disclosure: I hold a position in Pharos Energy plc (LSE: PHAR). This is not investment advice. Do your own due diligence.