Solitron Devices (SODI)

Small cap, missile defense beneficiary undergoing a strategic review.

Not investment advice: Read my full disclaimer here.

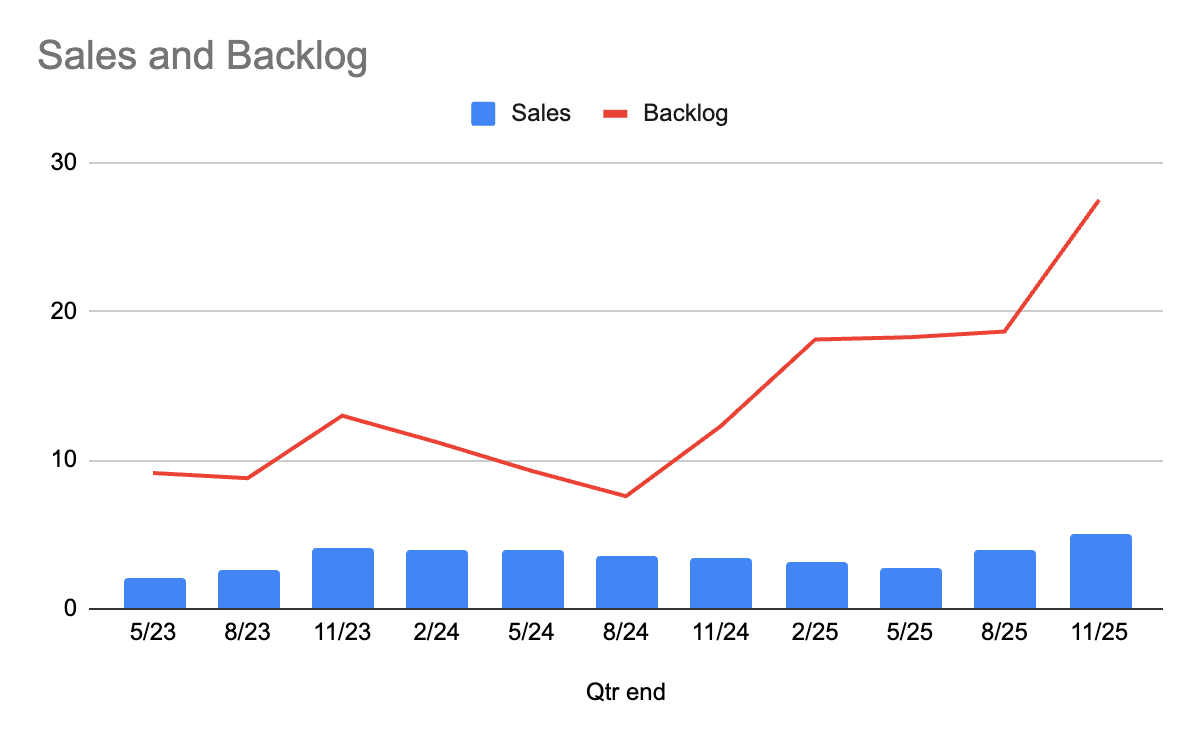

A 67-year-old West Palm Beach manufacturer of military spec power semiconductors, locked into AMRAAM and HIMARS production for the life of those programs, recently saw its backlog explode 124% year-over-year to $28+ million.

Solitron is a sole-source defense supplier. A company several tiers down the supply chain from the Primes that make military spec certified components that cannot be replaced mid-program without tearing up the qualification paperwork, re-running acceptance testing, and potentially delaying weapons production for a foreign ally in the middle of a war.

Solitron manufactures custom solid-state power semiconductors (transistors, MOSFETs, hybrids) for military and aerospace customers, headquartered in West Palm Beach, Florida. Its products are embedded in the AMRAAM air-to-air missile (Raytheon/RTX’s flagship), the HIMARS rocket artillery system (Lockheed/L3Harris), and a handful of other defense programs. It generates $14M in annual revenue on a trailing basis, has zero debt, and trades on the OTC Pink Markets with minimal coverage.

Here’s what has changed: 1) they announced a strategic review process 2) backlog exploded even before Operation Fury began.

Tim Eriksen, (head of Cedar Creek) went activist at Solitron about a decade ago. He is a great fiduciary of shareholder value and holds over 14% of shares outstanding through his fund and family investments. On February 3rd, he announced the commencement of a strategic review that could include a sale of the company. We should know more when they hold a delayed AGM next month.

At the end of the fiscal third quarter of 2026 (November 30, 2025), Solitron’s backlog stood at $27.48 million (up 124% from $12.28 million a year earlier). Bookings for that same quarter were $13.91 million versus sales of $5.02 million. The company now has 2x their TTM topline in backlog.

The Business:

Solitron was incorporated in 1959 and has spent six decades manufacturing high-reliability, custom-designed solid-state semiconductor components for applications where failure is not an option. The product lineup includes bipolar power transistors, power MOSFETs, power and control hybrids, and related devices. These are all produced to military specifications (MIL-PRF, MIL-SPEC) and certified to the Defense Logistics Agency (DLA) Land and Maritime standards.

These are not commodity semiconductors. You cannot substitute a commercial off-the-shelf part. Each component is custom-designed to a customer’s bill of materials, qualified through a formal DLA certification process that can take months or years, and then embedded into a weapon system for the life of that program. For major platforms, this often runs 20 to 40 years.

The products show up as critical power management and signal control components in:

Guided air-to-air missiles (AMRAAM / AIM-120)

Multiple Launch Rocket Systems (HIMARS)

Ground and airborne radar systems

Satellite and space applications

Power distribution systems for defense platforms

Missile control systems

The end customers purchasing Solitron’s components are the Tier 1 defense primes - RTX (Raytheon), L3Harris, and Lockheed Martin - who sell their weapons systems to the U.S. government and allied nations under Foreign Military Sales (FMS) contracts. Solitron’s products are effectively two steps removed from the Pentagon’s budget line, embedded in the bill of materials of some of the most in-demand weapons in the world.

The Moat:

When a defense prime like RTX designs the AMRAAM missile, they identify the components needed for the power management subsystem and work with a qualified supplier (in this case, Solitron) to develop and certify a custom semiconductor to their exact specifications. That certification is registered with the DLA. The part gets a specific NSN (National Stock Number). The weapon system’s qualification documentation references that specific component from that specific manufacturer.

Once a part is “engineered in,” replacing it requires:

Identifying an alternative supplier willing to reverse-engineer or redesign to spec

Running the new part through full DLA qualification (expensive, time-consuming)

Updating the weapon system’s technical data package

Potentially re-qualifying the weapon system itself if the change is deemed significant

Getting DoD and customer approval

For a component that might cost $50-$200 and represents a fraction of a percent of total weapon cost, no prime contractor is doing that in the middle of a production ramp. Once Solitron is in a program, they are likely in it for the life of that program.

This is also why Solitron’s revenue is sticky and its customer relationships span decades. The company has been a qualified supplier on AMRAAM for years. It was there before HIMARS became famous in Ukraine.

The Programs:

AMRAAM (AIM-120) — RTX / Raytheon

The Advanced Medium-Range Air-to-Air Missile is the backbone of Western air-to-air capability. Operated by the U.S. Air Force, U.S. Navy, and 40+ allied nations, AMRAAM is the primary beyond-visual-range air-to-air missile used by F-16s, F-15s, F/A-18s, and F-35s. The missile saw significant use in Ukraine in 2023-2024 through the NASAMS ground-launched variant, and demand from NATO allies and Indo-Pacific customers has been structurally elevated since Russia’s invasion.

The data points that matter for Solitron:

Raytheon CEO Phil Jasper, said: "Last year we doubled AMRAAM production; we're doubling production again this year, and we're going to continue to increase that production."

Solitron received the AMRAAM Lot 39 order during Q3 FY2026. Management noted the “order quantities were greater than the prior year’s order” and that pricing was also higher due to the “expiration of a multi-year pricing agreement.” This has yet to be reflected in margins (there is about a six month lag between receipt of an order and shipments).

Q3 FY2026 gross margin expanded to 34.3% from 29.7% a year earlier.

HIMARS (High Mobility Artillery Rocket System) — L3Harris / Lockheed

HIMARS became arguably the most famous conventional weapons system of the 2020s following its performance in Ukraine. Demand from European allies, Indo-Pacific customers, and U.S. Army replenishment has kept the production line busy. Lockheed Martin received follow-on HIMARS contracts multiple times within compressed timeframes in 2024, a sign of urgency in the procurement pipeline.

L3Harris is Solitron’s second largest defense customer. The large HIMARS-related order in Q3 FY2025 (ending November 30, 2024) was part of what triggered the initial surge in bookings. Lockheed’s follow-on HIMARS contract awards only a few months after the previous award. Supplemental orders to Solitron could continue to layer in throughout the production cycle.

SM-2, SM-6, and New Product Prototypes

The SM-6 (Standard Missile-6) is the U.S. Navy’s primary ship-based air defense and anti-surface interceptor, reportedly used or intended to be used to shoot down hypersonic missiles. Per Eriksen’s investor letters, Solitron’s Q4 FY2025 AMRAAM order from RTX is “believed to include parts for two or three years of SM-6 missile production as well” - meaning SM-6 components are already embedded in existing RTX production contracts, not merely a future prototype program.

As for SM-2, there is reason to believe this RTX program is ramping up as well. (example here)

Separately, management noted in the Q3 FY2026 results that it has “developed various prototypes for testing by potential customers” and remains “optimistic about creating additional revenue sources.” This language refers to new programs and customers entirely beyond the existing AMRAAM/HIMARS/SM-6 base. A successful qualification win on a new program would represent an entirely incremental revenue layer not in any current model.

// Here are some of the Investor Letters where you can start to put the pieces together:

Q4 2024 Annual Letter: Deepest SODI dive: HIMARS two-year order, AMRAAM at 1,200/yr, NDAA stockpile math, SM-6 embedded

Q1 2025 Letter: confirms $5M+ RTX/AMRAAM order, SM-6 embedded in that order, backlog $18.1M

Q2 2025 Letter: AMRAAM doubling is an “unfunded priorities list,” revenue timing trough analysis

Q3 2024 Letter: explains the Q2 FY2025 earnings miss (supplier scrapped 2,000 parts)

Q4 2023 Annual Letter: SODI +52% in Q4 2023, post-MEI adjusted operating income discussion

Management:

This is a company run by its largest shareholder, and that shareholder is a professional investor.

Tim Eriksen has been CEO of Solitron Devices since July 2016. He is also the founder and President of Eriksen Capital Management LLC and the fund manager of Cedar Creek Partners, a concentrated micro-cap value fund founded in 2006. Cedar Creek Partners holds approximately 11.6% of Solitron’s outstanding shares; Eriksen personally owns an additional ~2.5%. Combined, his economic interest in Solitron through his fund and personal holdings is ~14% of the company.

Eriksen’s background is atypical for a public company CEO. Before founding Eriksen Capital, he was an engineer at Kiewit, spent time in shareholder services at Franklin Templeton, and worked as an analyst at Walker’s Manual - a specialist in under-researched OTC companies. He has an MBA from Texas A&M. He brought capital allocation discipline and a long-term shareholder orientation that had been lacking.

Mark Matson serves as President and COO and runs the day-to-day operations. His background is deeply operational: COO and VP of Operations at YSI (instrumentation), VP of Operations and Engineering at Rockford Corporation, GM of the Seattle Division for Benchmark Electronics, and senior roles at ADIC and Interpoint - all precision electronics manufacturers. He knows how to run a facility that makes custom, low-volume, high-reliability components at MIL-spec standards.

Cedar Creek Partners has consistently featured Solitron in its quarterly investor letters as a high-conviction holding. His analysis of the business is more detailed than any external analyst could produce. He lives inside this company.

Valuation:

This is not a cheap company. At a $51.5M market cap, which is close to its EV, you’re not going to jump out of your seat to buy looking in the rearview mirror.

However, looking forward, the picture is very bright. Pick up their most recent quarterly and you can see the inflection is starting to reflect in the fundamentals:

Three months ending November:

$5M in revenue (+49%)

$653K in NI (+143%)

I think explosive growth will stay elevated. Backlog has grown exponentially. Pricing on some contracts has reset. Management is strong and squarely focused on driving shareholder value… which should result in strong operating leverage.

The future is bright…

Risks:

Here is my assessment of the material ones for Solitron.

Customer and Program Concentration: This is explanatory and known. AMRAAM and HIMARS represent the majority of Solitron’s defense revenue, and RTX appears to be the dominant customer. If either program experiences a production cut due to a quick resolution to the many ongoing conflicts - Solitron’s bookings and backlog would decline sharply once the replenishment drive ends. I do not forecast this would kick in for a long time.

MEI Customer Concentration (acquisition made in 2023): MEI’s dependence on a single medical customer for ~90% of its revenue is a vulnerability that Solitron inherited with the acquisition. Loss of that customer would remove a material chunk of company revenue. Solitron has not publicly addressed the status of this relationship in recent filings in a way that provides comfort around renewal risk.

Scale Limitations: Solitron has a limited number of employees and a single facility. Scaling production to meet a sustained AMRAAM doubling or new program wins requires capital investment in people, equipment, and potentially capacity. if you look at their LinkedIn, number of employees has not grown much and there are a lot of open jobs on their career page.

M&A: Mentioned as a potential avenue in the strategic announcement, I would be most concerned if they decided to buy another company. In this market, I’d like to be the beneficiary of the frothy defense valuations, not caught in buying and integrating an acquired entity. If that were the case, it’s likely either dilution would occur or the balance sheet would be burdened with debt. I find it highly unlikely Tim would fund a purchase with shares since he has clearly signaled they are undervalued.

Conclusion:

Solitron Devices is not a complicated story. It is a 67-year-old company with sole-source status in two of the most prominent weapons programs - AMRAAM and HIMARS. With a backlog that has exploded to nearly twice annual revenue at a time when the prime contractors supplying those weapons are publicly committed to production increases.

Most importantly, they are undergoing a strategic assessment by a strong capital allocator who is actively working to unlock the true value of this asset.

To quote what was stated on February 3rd:

“The process demonstrated to the Board that there is strong demand in the market place for defense related companies and that there could be numerous parties interested in acquiring the Company at a premium to the current share price or being acquired by the Company.”

This is a setup worth following closely.

Disclosure: I hold a position in Solitron Devices, Inc. (OTC Pink: SODI). This is not investment advice. Do your own due diligence.

Other notes:

Solitron will not pay income taxes until NOLs are used up. So cash earnings are higher. Any acquirer will be a tax payer unless it has NOLs.