Zoomd Technologies (ZOMD.V / ZMDTF)

Capital light compounder or value trap?

Zoomd Technologies has gotten interesting again. The darling of Canadian micro-cap land is now more than 50% off recent highs.

As a former owner/operator of a D2C company, I’m attracted to marketing technology (MarTech) companies that do something different. The spotty performance of these companies as a category has been due to a lack of product and service differentiation. Many of them are agencies masquerading as a tech companies. Historically, Zoomd was thrown in with a bad group of comparable companies despite offering real tech-enabled value. This was beginning to get appreciated, due to their stellar fundamental performance, before a Q3 top-line stumble.

What do they do?

Zoomd offers multinational programmatic advertising services. This is a fancy way of saying they find digital real estate to show ads to current and prospective customers of their clients outside the ‘walled garden’ ecosystem of social, search and soon, LLMs.

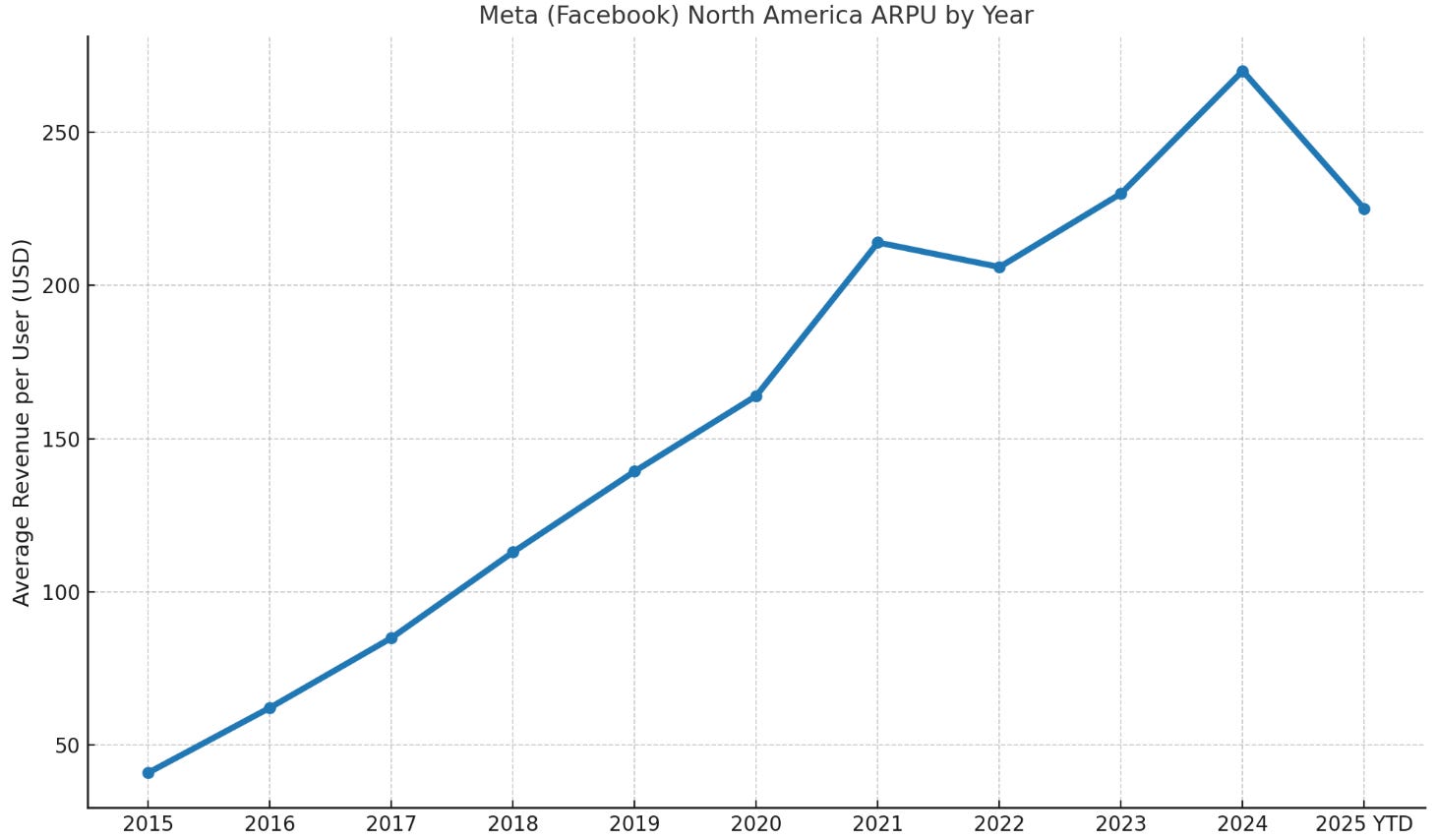

Post COVID, these walled gardens have largely been a race to the bottom. The number of advertising dollars chasing the same saturated eyeballs has skyrocketed. Take a look at Meta’s ARPU in North America. That’s up 6.5x in less than a decade!

Source: Financial filings. YTD ‘25 figure is not surprising, considering Q4 is their strongest quarter.

Furthermore, the transparency and target effectiveness of Meta were severely impaired by Apple’s decision in 2021 to allow customers the ability to opt out of data sharing. More specifically, Meta could routinely tie together your Facebook/Instagram activity and detailed actions in many other apps and sites on that device, at the individual level. Now when you select ‘ask app not to track,’ advertisers are not allowed to use your data for cross‑app tracking or user‑level ad attribution. Hence, Meta gets more dollars despite reduced efficiency. Who gets squeezed? Advertising customers.

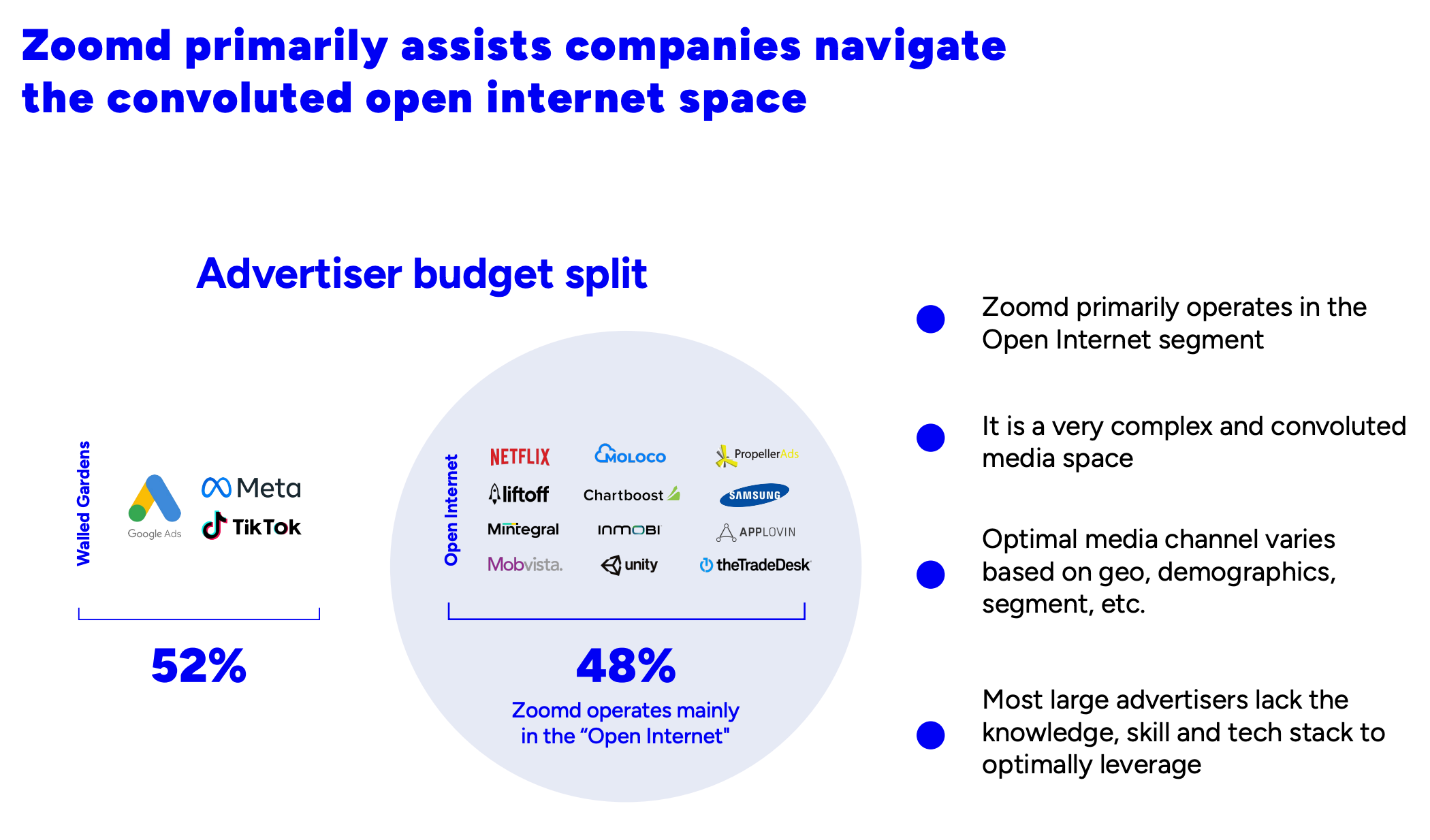

In turn, it provides a nice tailwind for Zoomd, which focuses on the rest of the internet - a segment that was historically under penetrated, just ask Applovin. Zoomd specializes in integrating into all the major ad networks with tech solutions that will place their clients’ assets (ads) where they can generate the highest ROI (e.g. app download, sale, etc.).

Source: Investor deck

Their Chairman, Amit, described Zoomd as pushing to become the ‘brain’ of digital marketing spend. With their vast connections across ad networks, they simplify a fragmented market by being able to allocate spend across 90%+ of global mobile traffic. This democratizes the marketing ecosystem and allows them to nimbly zero in on prospective customers - all summarized on their (one) platform.

To take a specific example, they may have an e-comm client that is targeting app downloads. Zoomd can approach this company and give them an alternative to acquisition on search, social, etc., without cannibalizing their core channels. This may be offered as a risk-free trial to start, where the customer pays nothing unless certain performance thresholds are met. If successful, the client could come on board as a long-term partner - finding another channel without expensive investment in an in-house marketing team. Further synergies are reached if the client is going after multinational audiences. Because of Zoomd’s deep reach and distribution network, they’re able to seamlessly find inventory across geographic regions (most of their revenue comes from fragmented Europe) to optimize returns. If one ad network, geo or creative type isn’t performing? No problem. They’re able to focus on those that are.

How does Zoomd make money? They arbitrage the difference between what the client pays for their desired action (purchase, app download, etc.) and the cost of placing their ad (the digital real estate). As an example, the customer may pay $50 for each purchase received from France on an Android. Zoomd’s goal is to get this acquisition for less than $30, to net a 40%+ margin on the transaction.

In some cases, this can lead to the cyclical performance that the market hates. This was the case in Q3 ‘25. Despite strong profitability, the top line was weak. In this case, two of their top clients changed their Mobile Measurement Partners (MMPs), which help define attribution, validating the source who gets credit for each action. This caused a temporary slowdown in volume. Management believes this will not have any long-term impacts, but it is a speed bump in Q3/Q4 2025.

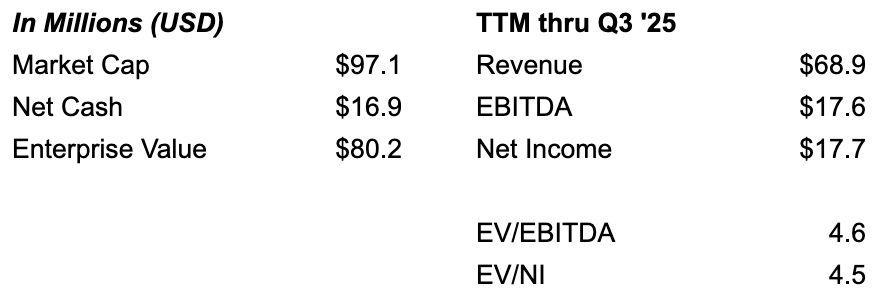

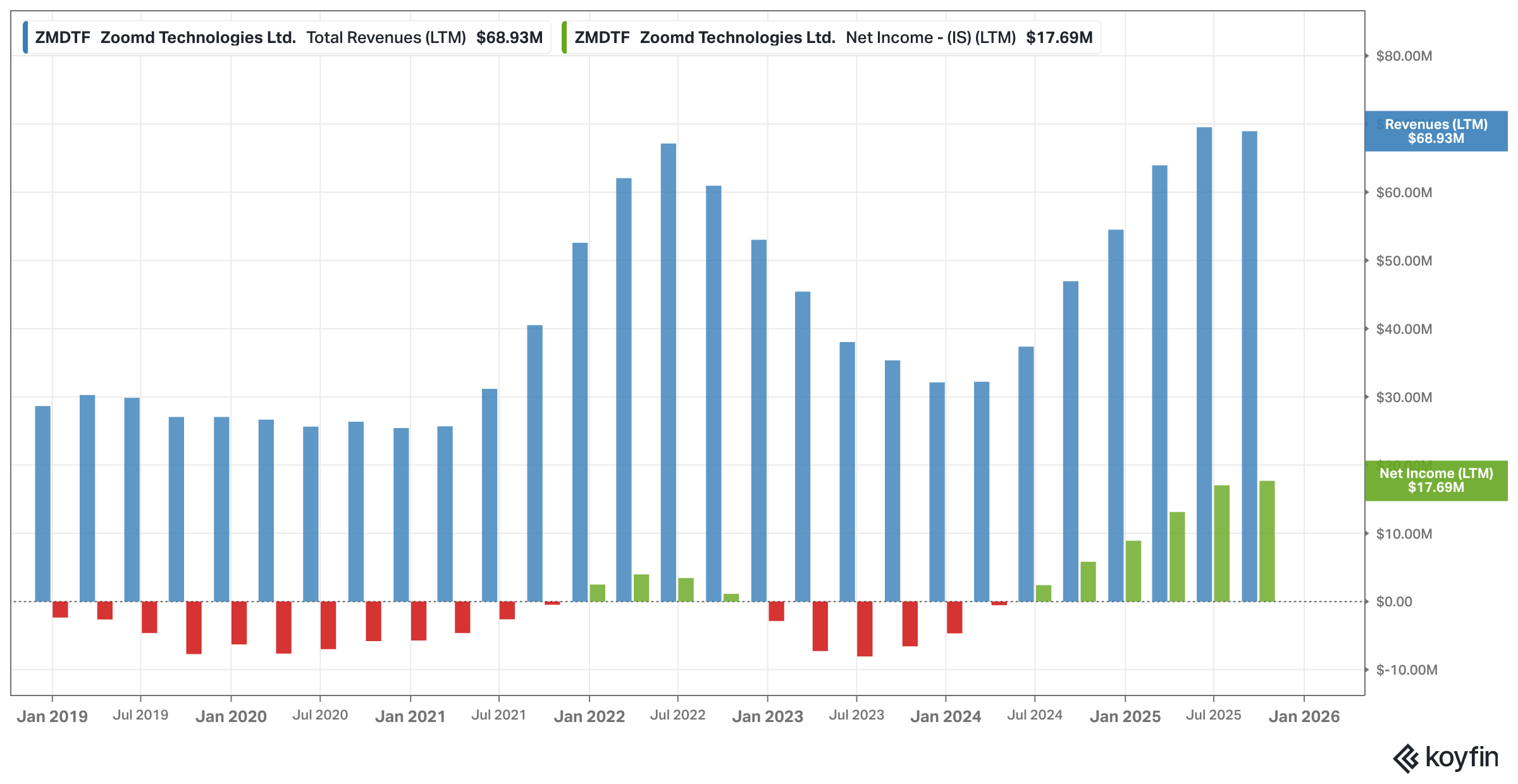

What is the valuation?

Source: Koyfin

This is where things get interesting! We are getting close to a 25% earnings yield (net of cash) on a trailing basis. You would think this was a cigar butt. Quite the opposite, Zoomd has turned into a cash generating machine, showing significant operating leverage over the course of the last 18 months. We’ve seen signs of life before. Will this time be sustainable?

Source: Koyfin

What are the catalysts heading into 2026?

Organic resolution of two of their top 5 clients changing MMPs (top 5 clients cumulatively account for 70% of revenue). As mentioned, management does not expect this to persist beyond Q4.

Outside the top 10, you had a doubling of YoY revenue. I’d expect this momentum to continue as they continue to successfully diversify from their top clients and have signed partnerships with the likes of E2. E2 is a marketer for many of the leading sports books (amplifying the bullet below).

World Cup: This should be a big tailwind to the company as many of their customers run increased dollars to this global event, which is 15x the EuroCup according to their Chairman. While it only happens once every four years, this should show a big result next year. (note: Winter Olympics are this year, as well)

Exchanges: Not my favorite way to create value, but a listing off the TSX to the Nasdaq makes a lot of sense. Right now the float breakdown is roughly 35% insider, 10% institutional and 55% free. That is a big retail position that has likely contributed to the share price volatility.

If this works out as anticipated, a strong 2026 is in the cards.

Something to keep a close eye on is operating leverage. A theme over the last couple of years has been a pivot to focus on the core money making activities (enterprise), while leveraging technology (e.g. creative machine learning), reducing the need for additional headcount. Moving forward, unit economics are important to monitor. If you see a reduction in profitability, that could indicate a slippage in their arbitrage spread, potentially reflecting a reduced competitive advantage.

What could go wrong?

The risk this is a value trap…

Competition: This is a ‘red ocean.’ There are lots of competitors that serve as alternatives to Zoomd. In fact, many of their ad network partners are also competitors. The most well-known one, is Applovin, which has been very innovative in their tech development - with AI-driven campaigns, a huge SDK network and an ad exchange (MAX).

Customer Concentration: With 70-80% of revenue generated by their top 5 customers, losing one account would leave a huge hole in financials. The good news? Most are longstanding customers.

What gives me further pause is the recent hiccup in Q3 revenue. H2 is a seasonal high point for consumer brands. Therefore, why would two of their top 5 clients make such a large, fundamental change at this time? Is this transitory, or a sign of a strategic pivot?

Going back through their 2019 reports, Zoomd had similar concentration. However, several of these companies are no longer using them. “The Company has global operations and provides services to top tier brands such as PokerStars, Shein, 90Min, Alibaba and Bwin.” Source: 9/30/19 MD&A. Churn moving forward is a major concern.

Capital Allocation: It will be very interesting to see how their cash generation is deployed. Candidly, I am worried about Zoomd going out and expanding by acquisition. Speaking with the Chairman, I believe most of this would be done to grow the customer base (‘buy the book’ if you will). However, if the product is that superior, why would that be necessary versus approaching them organically or through partnership?

If there is strong belief in the future prospects of this company, a buyback would be an obvious choice (retiring shares at a 25% earnings yield). Then, why not dividends with the capital light nature of this business? There are so many companies that stumble when they go from turnaround to capital allocator. Hopefully, Zoomd is not one of them.

Focus on Stock Price: Amit (Chairman) is keenly aware of where the stock trades. He makes himself very available (appreciated) and has a sentiment pulse on individuals who could have a positive impact on the stock. He was especially active prior to Q3 earnings. Why is this taking up so much mindshare? I don’t have an answer, but it worries me.

The Long-term Opportunity

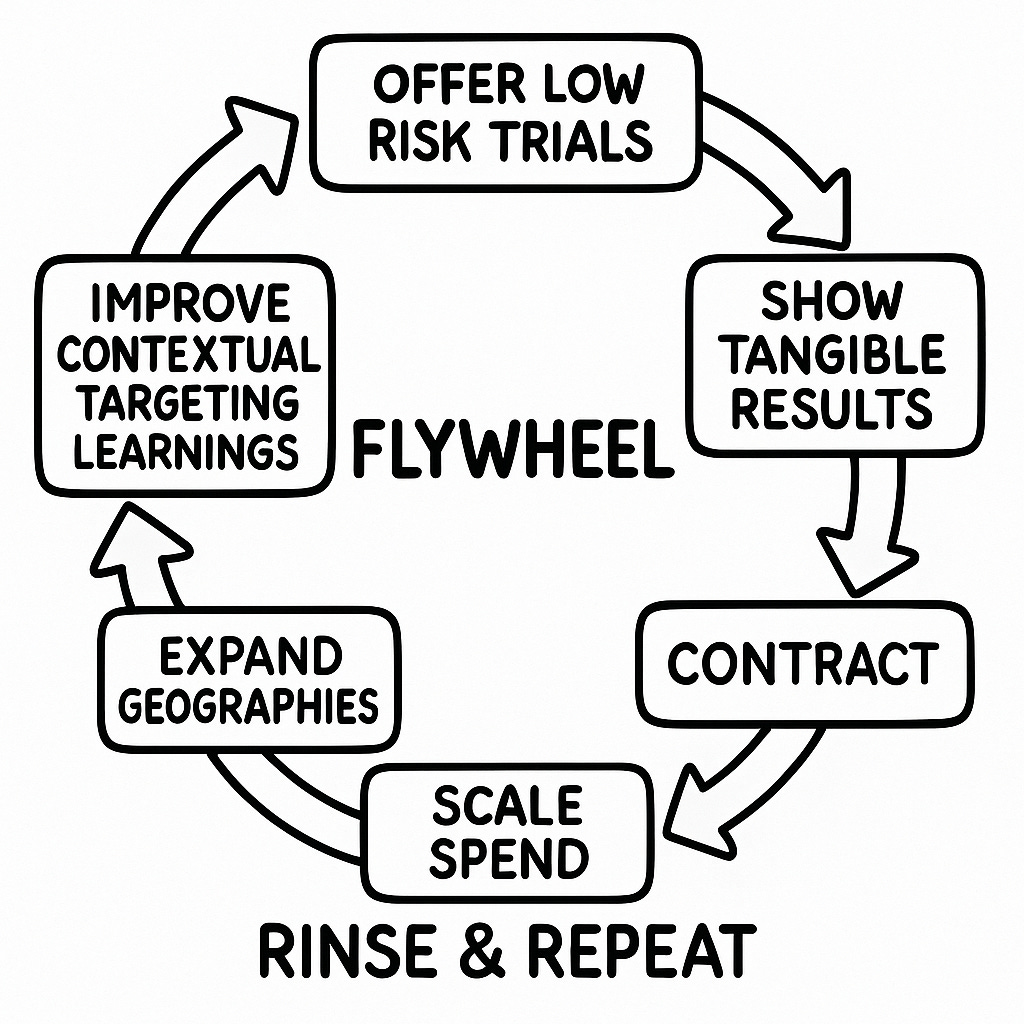

Long-term, how does the company continue to grow and generate strong returns for shareholders? They produce results. Revenue being up over 100% year-over-year from clients outside their top 10 is indicative of their strong value position. They have developed a nice business development flywheel:

Furthermore, Zoomd has done a great job of penetrating a diverse array of industries and large multinational clients. In broadening these relationships, they have enhanced their understanding of what works, allowing them to apply these learnings to sell to future clients and generate results for them.

Zoomd’s moat is a global distribution network that is being broadened through the depth and breadth of their consumer data and insights.

This global distribution network is leveraged to find the best creative and placements based on campaign parameters. In turn, they are sending real-time insights back to their clients to tweak future creative assets in ways that will further improve their performance.

Source: Value Bridge

My expectation and hope is that this will continue spinning, generating results across their book of business. With that said, coming up with a perspective on future cash flows is very difficult due to the competitive nature of the industry and low switching costs.

Note: This is a great internal article to get to understand their perspective and presence re: user acquisition trends.

In Summary

AN INVESTMENT IN ZOOMD IS NOT FREE MONEY. Behind the shiny earnings yield, there are a lot of large risks. This is a viciously competitive industry with low switching costs and a lack of recurring revenue. If a company like Shein goes elsewhere (which I estimate to be >25% of revenue), watch out. Similar events like this have happened in the past, like when live events went dark in 2020 or crypto.com pulled back spend without much warning.

With that said, I remain an investor in the stock. Why?

Zoomd Technologies has executed a fundamentals based turnaround. Their continued focus on bottom line strength proves they are serious about rewarding shareholders. I do not think it is a coincidence this happened soon after the former head of Amex Israel became CEO.

Misunderstood by many, their business model has economies of scale and generates tangible results for their clients. This is exemplified by the quality of businesses that are partners, significant growth from those outside the top 10 and their regular deepening of partnerships across a diverse range of industries and geographies.

Buying shares in the company after a relatively weak Q3 ‘25 could offer a good entry point, especially if you believe the company will grow in 2026 (as I currently do).

Appendix

The brands Zoomd serves are top notch.

However, there is Discretionary Income / Recessionary Risk: Primary end markets of Zoomd are sensitive to changes in disposable income (in my opinion). Their top industries by revenue are e-comm (42%), entertainment (25%) and gaming (12%).

My history with the company: I bought shares after finding them at a MicroCapClub conference in April at an average price of ~$.70 CAD. Before they announced Q3 earnings, I reduced my holdings by ~35%.

Do your own due diligence. Any investment has the potential to fall to $0. I own shares in this company. Therefore, I am biased toward their success. All information should be double-checked, as it could be wrong.

Yeah, it’s an interesting risk/reward. I don’t think the Q3 was churn per se, just lower volume on a couple of their top 5.

Really not much change in the last 60 days. Definitely not enough to warrant a 50% drop, but it exposed some vulnerabilities.

Excited to see what they can do with the Olympics and World Cup. Those are strong numbers they’ll be lapping by then.

Given that a lot of their business comes from Shein plus EU, I believe that the negative pressure on the stock is not only due to the slight decrease in revenue (q3) but also this:

https://www.consilium.europa.eu/en/press/press-releases/2025/12/12/customs-council-agrees-to-levy-customs-duty-on-small-parcels-as-of-1-july-2026/