iOCO: Deep Value with a Compounding Playbook

Rhys Summerton is executing his serial acquirer playbook in a capital light industry.

Not investment advice: First, read my full disclaimer here.

The value investor who helped engineer Argent Industrial’s transformation and took control of Aimia is now the CEO of a R5.7 billion revenue JSE tech company trading at ~5x EBITDA. Working for no salary, consistently buying back stock, and predicting four to six acquisitions a year at 4-5x earnings.

If you haven’t already, check out my previous article that covers Rhy’s involvement at Aimia and Argent. Rhys, the former Citigroup Global Head of Emerging Market Equity Research who founded Milkwood Capital and whose engagement with Argent’s management helped spark one of the great compounding stories on the JSE.

I expect this playbook to be Argent 2.0 - except in a capital light industry. So what happened at Argent under Rhys involvement?

Milkwood disclosed a stake of 20.4% in Argent in October 2017, and Summerton’s active engagement with CEO Treve Hendry’s management team began in 2018. The engagement centred on two things: stop accepting low returns on capital in a depressed home market, and treat your own discounted shares as the best acquisition available.

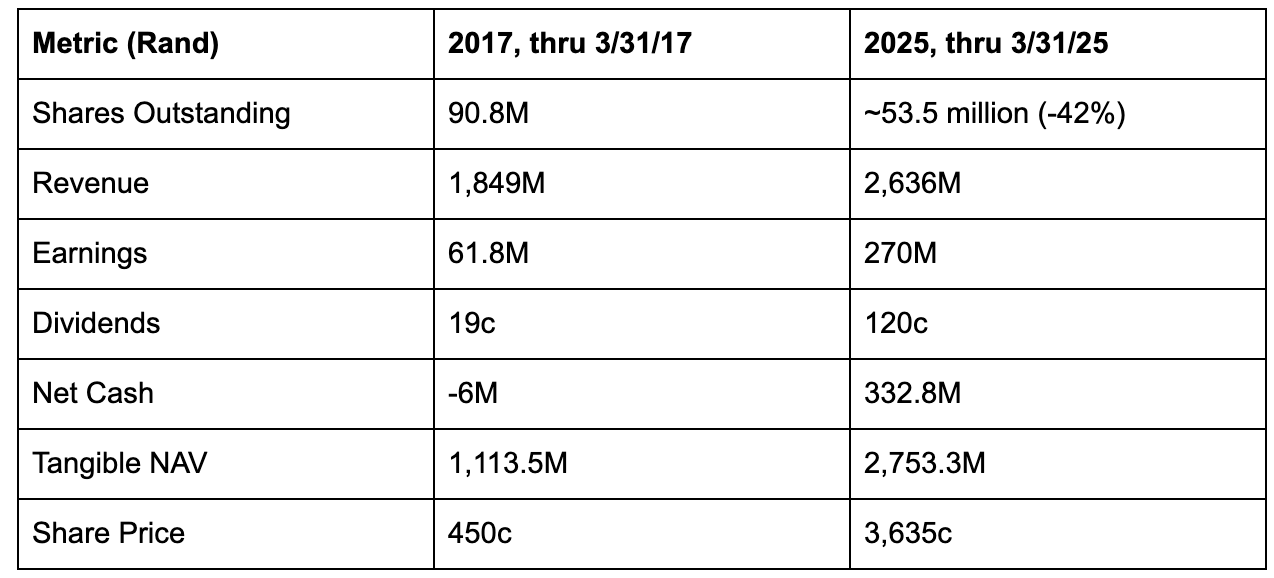

Here’s what happened at Argent over the period of Milkwood’s involvement:

Argent repurchased more than 40% of its own shares over the period. It compounded EPS at roughly 30% a year over six years, with about three-quarters of that from operational improvement and a quarter from the shrinking share count. Anthony Clark at Smalltalkdaily ranks Argent a top performer on the entire JSE over 2015-2025 at roughly 27% per annum in total returns, ahead of darlings like Capitec on his value-growth measure. A rand invested alongside Milkwood’s engagement is up over 7x, not including dividends.

Acquisition discipline, the carryover most relevant to iOCO, was strong. Argent set a ceiling of 6x earnings on acquisitions and consistently came in under it: OSA Door Parts for £2.5 million in 2016, Fuel Proof at roughly 4x in 2018, Fluid Transfer - a leading UK aviation refuelling manufacturer now exporting to 81 countries - for a nominal £1 from a distressed seller in 2021, and Standmode/Mersey at 4.9x earnings in 2024. No debt, funded from cash flow.

That is the playbook Rhys likes: buy back your own stock relentlessly while it’s cheap, acquire niche businesses at multiples so low the deals are nearly impossible to lose money on, keep the balance sheet debt free, and let the virtuous circle do the compounding. Argent proved it works on the JSE, in an unloved sector, with a South African discount hanging over the stock the entire time.

Now transpose it to iOCO, what’s different? Argent is a manufacturer: working capital, factories, steel inputs, freight, equipment. iOCO is a technology services business. As Summerton put it in an October 2025 interview: “You have no capex in this business, so EBITDA should translate directly into cash.” The FY2025 numbers back him up - 53 cents of free cash flow per share against 40 cents of HEPS. The asset-heavy version of this playbook produced a seven-bagger. iOCO is the asset-light version, run by him as the CEO.

Of all Summerton vehicles, this is the one I consider the most attractive.

iOCO Limited (JSE: IOC) is the company formerly known as EOH Holdings: once South Africa’s largest home-grown technology services group, then the protagonist of one of the most spectacular corporate implosions in JSE history, and now - after seven years of painful repair work - a clean, debt-light, cash-generative IT services business doing roughly R5.7 billion in revenue. In May 2024, Summerton joined the board. In February 2025, he became joint interim CEO, taking no cash salary, with his compensation tied entirely to the share price. Since February 2026, he has been the sole CEO.

At Argent, Summerton was an engaged shareholder - influential, but technically outside the C-Suite. At Aimia, he is Executive Chairman of a holding company. At iOCO, he is the chief executive.

If you haven’t already, I recommend you first read my overview of Aimia. During their AGM they outlined five companies entitled ‘Sample Target Investments.’ I outline who I think these could be. Now that Aimia has cash from a recent asset sale, they could turn into an acquisition.

The core thesis: iOCO is a turnaround that has already begun to inflect. FY2025 EBITDA grew 68%, the company swung from a headline loss to 40 cents of EPS, and H1 FY2026 delivered the first organic revenue growth in years. Now the Rhys Summerton playbook begins: aggressive buybacks below intrinsic value, bolt-on acquisitions at 4-5x earnings in a fragmented market with few other consolidators, and a stated medium-term target of R500 million of free cash flow over 500 million shares. You’re paying roughly 10x trailing earnings, under 5x forward EBITDA, and about 7x guided free cash flow for it. If the serial acquirer model works, the multiple won’t stay there. If it doesn’t, you own a 15% free cash flow yield being returned to you through buybacks.

Let’s dive in and see why I’m so excited about this opportunity.