Kidoz (KDOZF / KDOZ.V)

Poised for a strong finish to end the year.

*Amounts are in USD unless otherwise stated.

As I mentioned in my article about Zoomd, it’s fun to find investments in a beat-up industry where good companies are thrown out with the bad. Enter Kidoz, an ad tech company that generates the majority of its revenue by helping brands target children under 13. Originally, I was going to pen this as a paid article under the title ‘My Favorite Q4 Investment.’ Now, with the stock price up 90%+ in the last three months, I think the easy money has been made. However, I’ll give you the details so you can reach your own conclusions.

The internet is, in essence, real estate that has billboards plastered all over it. Companies have been ingenious in how they have used this to enrich themselves, especially the ‘walled gardens’ of Meta, Google and TikTok. They leverage their ability to capture consumer attention, understand who that consumer is based on a mind-numbing array of behavioral/contextual data, and sell access to advertisers that place campaigns and ads within their ecosystem. It is an incredible business model if you have the network effects to put it all together.

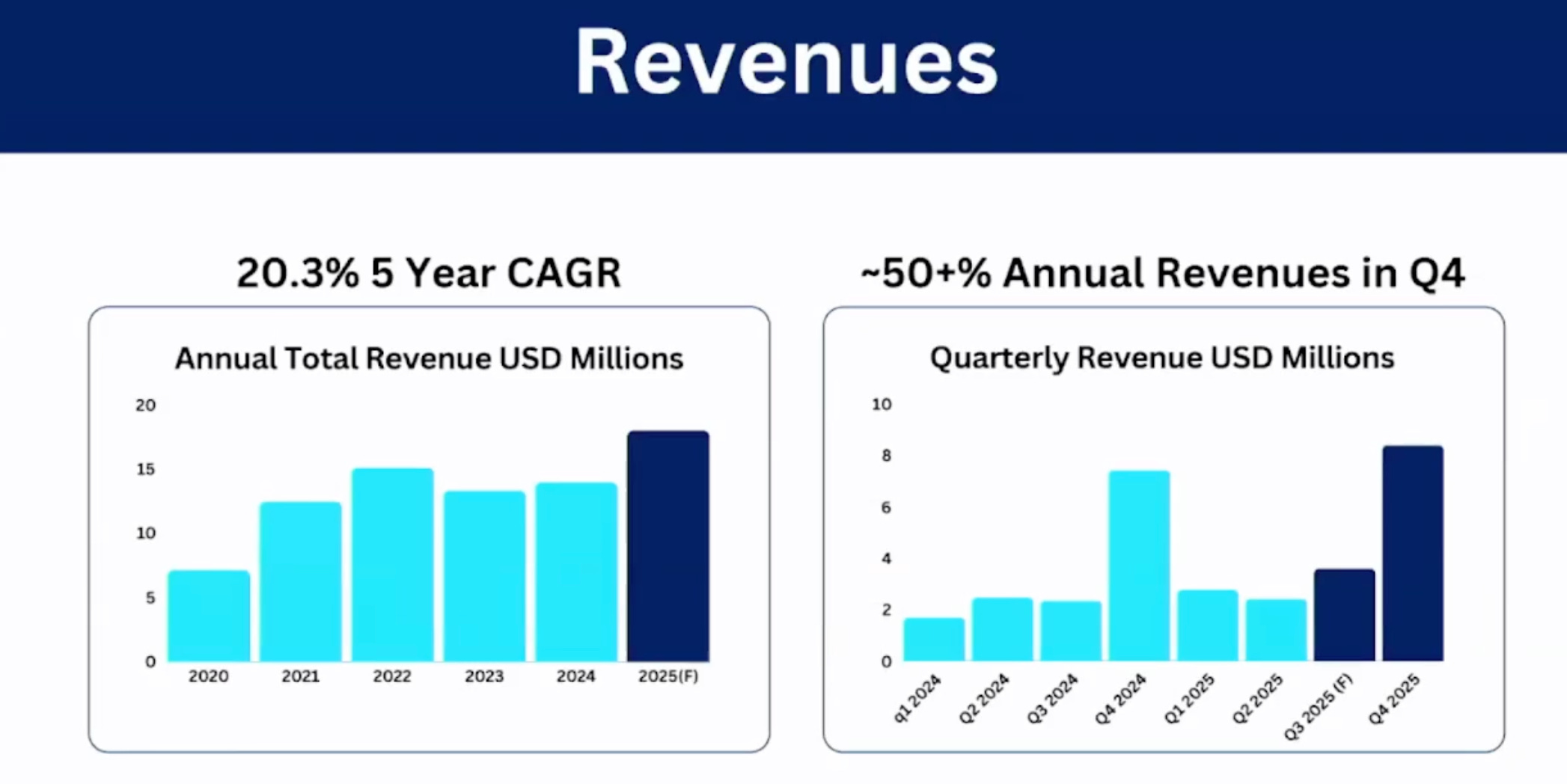

As it pertains to Kidoz, it has built the direct client relationships, proprietary technology and (most importantly) targets a demographic that has been underrepresented by competitors in any meaningful way. What caught my attention was a slide in an October Toronto (Planet MicroCap) presentation where they telegraphed 75% of revenue coming in H2 after a choppy start to the year. With a 60% year-over-year revenue increase in Q3, they are on target to do $18M+ this year.

Source: TOR Planet Microcap Conference

What do they do?

Kidoz provides a way for brands to contextually target customers. This means it does not require a specific location or personal identifier and is fully COPPA (Children’s Online Privacy Protection Act) and GDPR-K (GDPR for Kids) compliant. How they work with their clients - which include McDonald’s, Mattel and Lego - has evolved and deepened over the years. But here is an example of how it works.

Mattel (their largest client) wants to target children under 13 in a brand safe, COPPA-compliant manner. What that means is:

No user-level tracking

No cookies or mobile IDs for ad personalization

No re-marketing, lookalikes, or profiling

Contextual ads only.

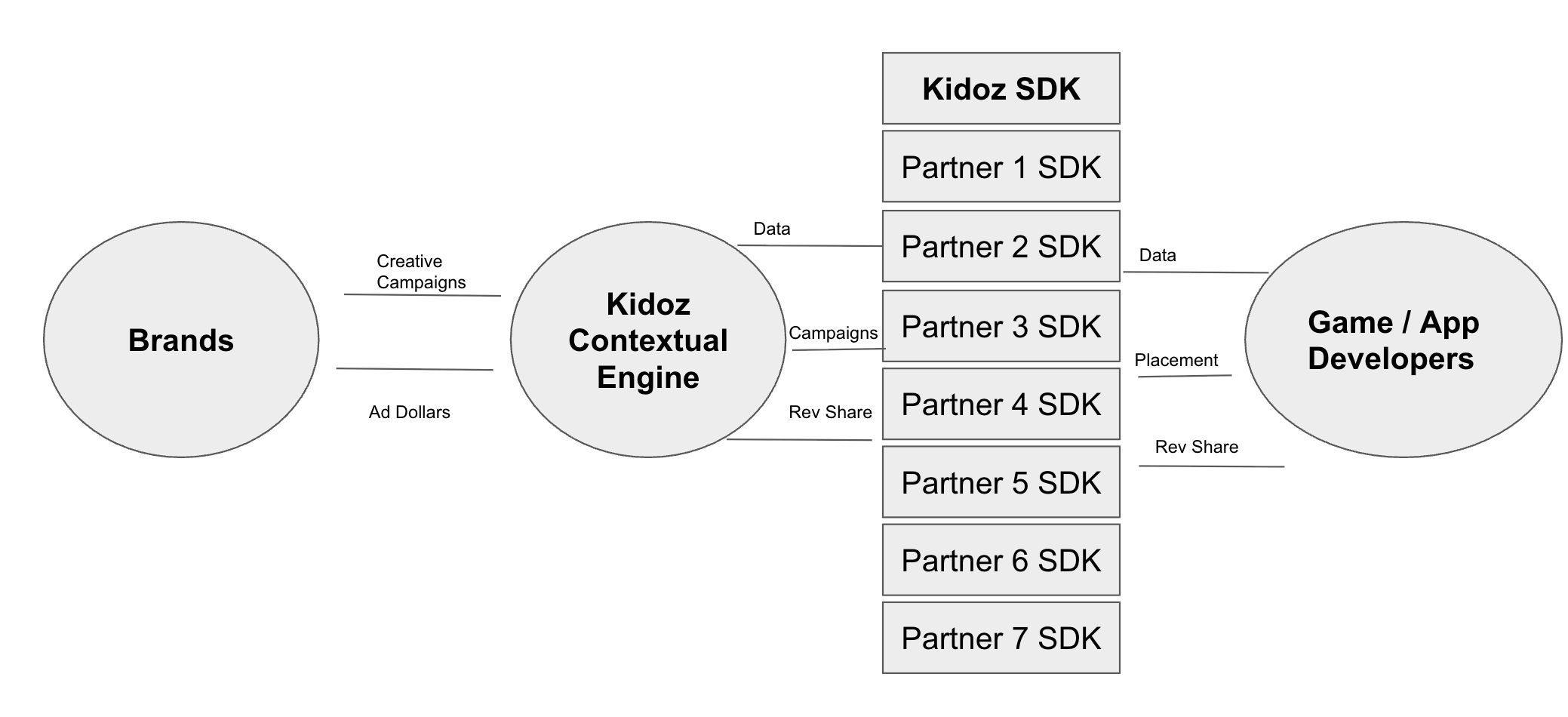

The rules they play by for older audiences do not apply here, and they need to do things differently. That creates the business opportunity Kidoz saw and works to solve by enabling contextual information gathering and targeting within mobile apps. They are able to get access to these apps (mobile games being 90%+ of where their ad dollars go), via direct relationships as part of their own Software Development Kit (SDK) or through the seven additional SDK partners they work with. Therefore, when running a campaign on behalf of a client, there are a lot of options they can use to find the best ROI.

A specific campaign example is a partnership they did with McDonald’s earlier this year. In this case, the target were Spanish-speakers within the United States. As part of the partnership, Kidoz produced the ad assets and harnessed their targeting technology to reach the desired demographic, allocating spend across mobile applications (again, primarily games).

Here is my understanding of the business model:

I believe Kidoz creates significant value by identifying the games that their target audience (children under 13) play. Once those are identified, they go directly to the developer and try to get them integrated into their SDK. If they’re lucky, that developer will not have a lot of SDK relationships. This creates a less efficient marketplace, making the cost of ads to place in their app ecosystem less competitive. Hence, Kidoz is able to pay a lower price and pocket the difference charged to their customer.

Earlier this year, Kidoz invested in building out their age 13+ contextual platform called Prado. This gives them an option to offer broader advertising services for clients moving forward. If there are regulatory tailwinds behind contextual ads (you can imagine how fragmented rules currently are across geographies), Kidoz will be in a prime position to benefit.

Furthermore, Kidoz has already spent the development ad dollars that will allow significant scale of their current platform. Think of it as building out an architecture (the “plumbing”) that can handle multiples of their current volume. If they are successful in growing out and saturating their customer base, they should demonstrate strong operating leverage.

What is the valuation?

In recent years, Kidoz has demonstrated strong growth. Similar to most brands in the direct-to-consumer ecosystem, they especially did well through COVID. While there was some impact as the tide went out in 2022, it was largely a reflection of the industry, more so than any operational mistakes. What makes it all the more impressive is the fact they were able to take their revenue streams from being reseller dependent to in-house direct relationships.

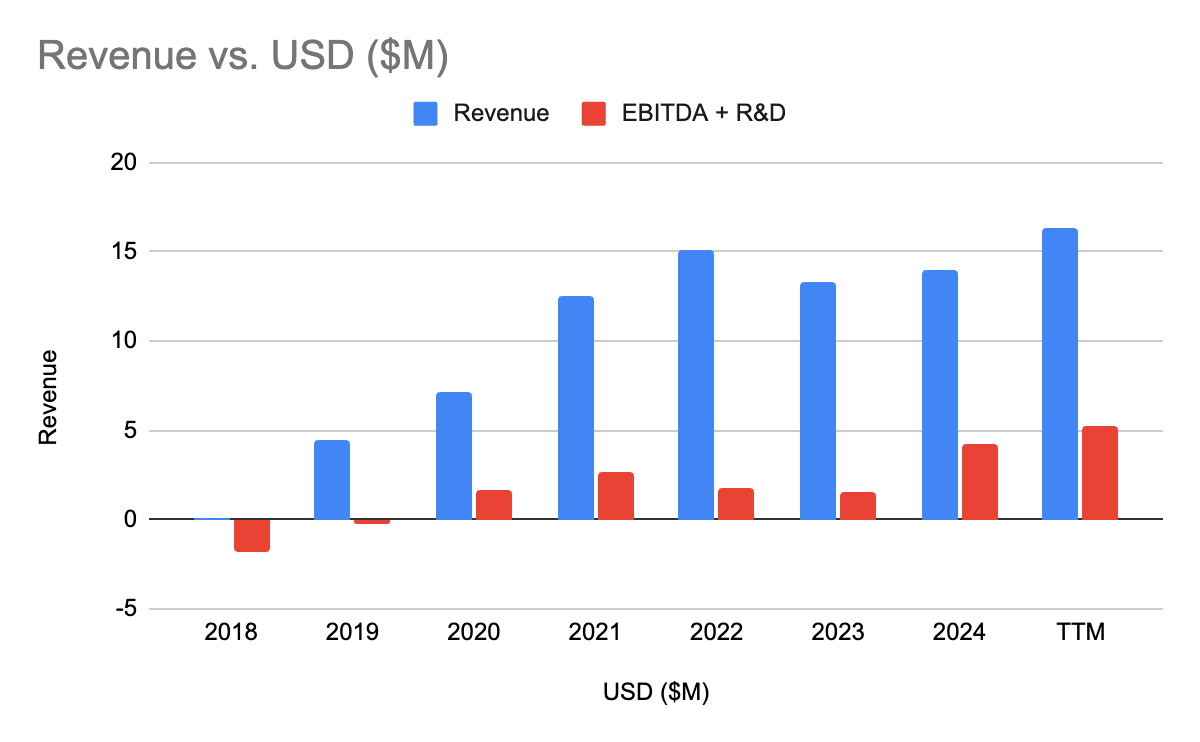

An interesting thing about Kidoz is that they expense all their R&D costs. That means if they are enhancing or building a new product, all the development expense associated with that build hits the P&L. Meanwhile, the useful life of the developed product can be measured in years. Here is what profitability would look like if you removed R&D expenses:

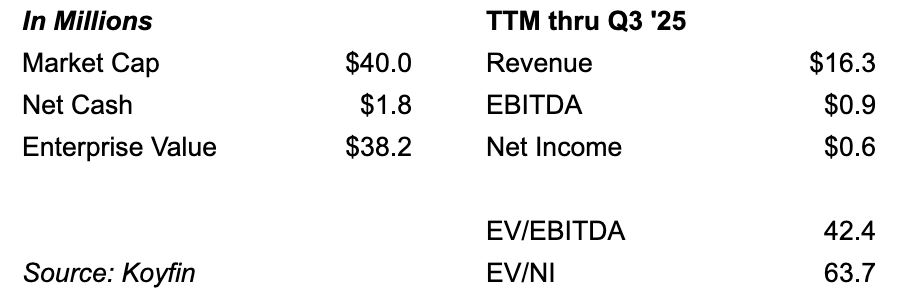

Source: Koyfin

Look, it’s easy to fool yourself with non-GAAP financials. The reality of their true profitability probably lies somewhere between EBITDA and EBITDA + D&A. If you take this adjusted value, Kidoz did $5.3M in adjusted profit, which is 7.5x EV/AEBITDA. I expect this number to improve nicely after Q4, which has been guided to be a record. Additionally, there was a net working capital balance at the end of Q3 ~$3M that should turn into cash over time.

So what does the competitive landscape look like? According to CEO Jason Williams, direct competitors are limited. A company named SuperAwesome previously developed great technology. It was purchased by Epic Games and he mentions it’s unclear if they are still building their kid-friendly product.

The bigger risks are the major incumbents (e.g. Google, Apple, AppLovin) stepping up and having their own contextual targeting solutions. In that case, advertisers could go directly to these large players and safely target their desired audiences without the need for Kidoz. That would be the true test of whether the millions spent have created a defensible moat. What are these large players doing today? They are not targeting children. Too much regulation and problems could arise that are not worth disrupting or losing focus on their cash cows.

Here is an overview of the various channels available to a brand and the competitive landscape.

— Walled Gardens: Facebook, Instagram, TikTok, etc. If you self identify in the under-13 audience, you’re not allowed on their social platforms (per COPPA) or have to operate within restricted parameters (in the case of TikTok).

— Open Internet: Web browsing doesn’t get a lot of volume from children under 13, and isn’t a big competitor, according to Jason.

— In-app marketing: This is where Kidoz focuses, targeting games those under 13 use. A major player like AppLovin does not allow targeting of children. However, a movement by Supply-Side Platforms (SSPs) to come up with their own capabilities could bring serious competition.

— Video/CTV: This is a primary competitor. The likes of YouTube and children’s based programming (e.g. Happy Kids) is extensive and specifically targeted at the same audience.

What are the risks?

— Result orientation: There is a ton of gray area in the digital advertising space, especially as it relates to kids. Even if the regulation exists, compliance with mandates is hard to monitor and rare to enforce. The unfortunate side effect of investing in Kidoz is that its contextual data does not enable the targeting efficacy or attribution tracking of the behavioral solutions. It’s hard to compete against a competitor that utilizes data that encompasses everything you do on your cellphone to target their ads.

— Customer concentration risk: Jason mentions there are around 20 clients who are large enough and interested in safely advertising to the under 13 audience. Needless to say, that brings with it great concentration risk, unless regulation and enforcement make their tech necessary. Three customers are driving the majority of revenue for the company right now - Mattel, Lego and McDonald’s. The good news is there is a lot more saturation that could occur within each. I get the sense that Lego could be the big story in 2026.

— Profitability: Jason’s vision is to grow profit year over year in aggregate, but not necessarily target certain profit KPIs (e.g. 15% NI margins in 2026). I get it from his point of view, if he has ways to deploy the capital. However, as an investor, you need trust in management. I’m too new here to have formed that perspective yet. My biggest red flag came where I asked him about the development milestones for ‘single-digit’ increases in R&D spend (over $5M) in ‘26 and didn’t get a clear response.

— Promotion: Kidoz has become more promotional with the hiring of a contracted IR representative and a market maker. Short-term, I view this as a bullish indicator, potentially reflecting their belief that they have a provocative story to tell (for the IR hire, at least). However, that is a significant and unnecessary cost burden for a $40M market cap company.

In Summary

Kidoz has done a great job growing their business over the last seven years. They saw an unexplored piece of the market - in-app advertising to children - and went after it.

As an owner of the business now, you are getting the rewards of having $20M+ in non-capitalized R&D expenses. This has given the appearance of poor fundamentals, covering up the true strength being shown by the organization via a much better product and moving from reseller to direct client relationships.

Longer-term, I think the following drivers will be tailwinds for Kidoz:

Regulation is going to become more stringent in the future. Contextual > behavioral targeting is where the puck is moving. Australia is actively moving to block social media access to teens (good luck).

Establishing direct relationships was a painful, but necessary step for Kidoz to take. They’ve replaced $9M in reseller revenue with $12M of direct brand revenue (higher margin), which will continue to pay dividends. This direct relationship has the Kidoz create a lot of the creative assets they’re displaying on behalf of their clientele - creating more of a full-service offering.

The Kidoz contextual platform is built to scale and should let this business show strong operating leverage moving forward.

For me, I’m likely to remain a shareholder until Q4 results are announced before making a longer term decision.

A summation of AdTech

Small-cap, non-recurring-revenue, ad-tech companies deserve to trade at a discount to the market.

They operate in a red ocean dominated by multitrillion-dollar companies that depend on digital ad revenue for the cash flows that fuel their businesses (see: AppLovin, Meta, Google). While small cap companies like Zoomd and Kidoz occupy interesting niches, you have to be very careful to make sure they are not disrupted or displaced by the large incumbents or scrappy upstarts. This makes long-term predictions about their free cash flow exceptionally difficult. This unpredictability warrants a discount and close monitoring while you own the securities. Be careful out there and always remember the mantra - buy low, sell high.

This is not investment advice. Do your own due diligence. Any investment has the potential to fall to $0. I own shares in this company. Therefore, I am biased toward their success. All information should be double-checked, as it could be wrong.

Absolutely, evaluating the underlying value of a business like Kidoz can be quite complex, especially when considering the importance of network effects in their model. I've found that doing thorough due diligence is key—it's great to hear that you emphasize that. Personally, I’ve been using a tool called DREA (Digital Real Estate Analyzer) to help assess various digital assets; it’s been a game-changer for organizing my thoughts and data. Good luck with your evaluation!